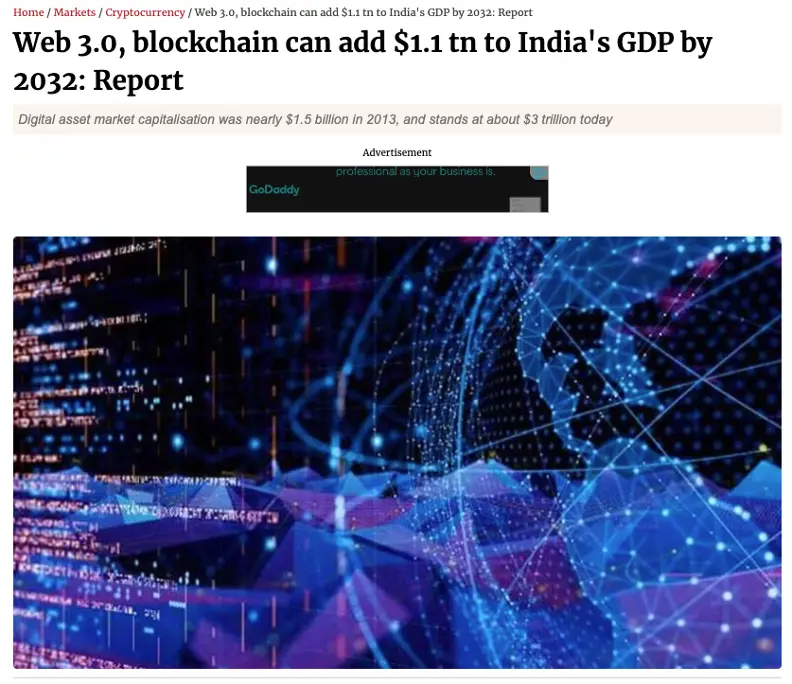

The crypto economic impact on India could reach $1.1 trillion in GDP contribution by 2032 — and that estimate predates India's mutual fund industry crossing Rs 73 lakh crore. Blockchain GDP in India is projected to grow at 43.1% CAGR. A CrossTower-USISPF report projects the digital asset economy's value to India's GDP will grow at 43.1% CAGR from $5.1 billion in 2021 to $261.8 billion annually over an 11-year period. India ranks #1 on the Chainalysis Global Crypto Adoption Index with 119 million crypto owners. Yet it has zero regulated crypto mutual funds.

This article does what policy discussions rarely do: model the actual numbers. What happens to tax revenue, job creation, startup investment, and India's global positioning if even a fraction of the mutual fund industry's capital enters regulated crypto? The answer is not speculative — it is arithmetic.

Source: Business Standard / CrossTower-USISPF Report, December 2021

The Numbers That Frame the Opportunity

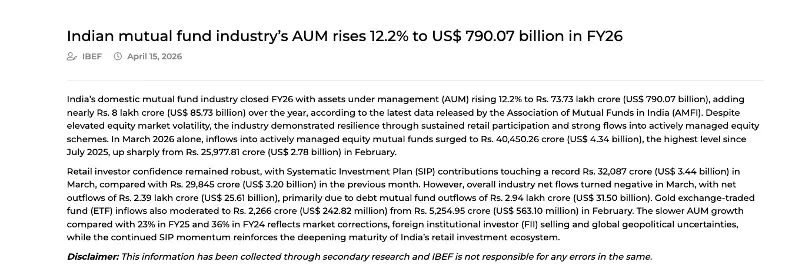

India's domestic mutual fund industry closed FY26 with AUM rising 12.2% to Rs 73.73 lakh crore (US$ 790.07 billion), according to AMFI. This is a six-fold increase from Rs 14.22 trillion in April 2016 — a decade of compounding driven by SIP adoption, tax incentives under Section 80C, and rising financial literacy.

Systematic Investment Plan (SIP) contributions touched a record Rs 32,087 crore ($3.44 billion) in March 2026 alone. The industry added 34 lakh new folios in March. Retail participation is no longer a niche behaviour — it is a national financial habit.

Source: IBEF / AMFI — Indian Mutual Fund Industry AUM, FY26

Now consider the other side. India processed $2.36 trillion in cryptocurrency transactions between July 2024 and June 2025 — a 69% year-over-year increase. The country has millions crypto owners, more than any other nation. 72% of these investors are under 35. The demand is not theoretical. It is already here, flowing through unregulated channels.

The 2-3% Model: What If MF AUM Entered Crypto?

Here is the core calculation. If 2-3% of India's mutual fund AUM were allocated to regulated crypto mutual funds, the numbers look like this:

Metric | Conservative (2%) | Moderate (3%) | Context |

MF AUM Allocation to Crypto | Rs 1.47 lakh crore | Rs 2.21 lakh crore | Total MF AUM: Rs 73.73L Cr (FY26) |

Equivalent in Global Context | ~15% of US BTC ETF AUM | ~23% of US BTC ETF AUM | US spot BTC ETF AUM: ~$114B (Nov 2025) |

Annual Management Fees | Rs 2,210 crore/year | Rs 3,315 crore/year | Revenue for AMCs + distributors |

Annual Tax Revenue | Rs 6,630 crore/year | Rs 9,945 crore/year | vs Rs 511 Cr TDS collected FY25 |

New SIP Folios (est) | 40-60 lakh | 60-90 lakh | At avg Rs 3,000-5,000/month SIP |

Note: Projections based on stated assumptions. Actual outcomes depend on regulatory framework, market conditions, and investor behaviour. Past performance of crypto assets is not indicative of future results.

India's Crypto Adoption: #1 in the World, Zero Regulated Funds

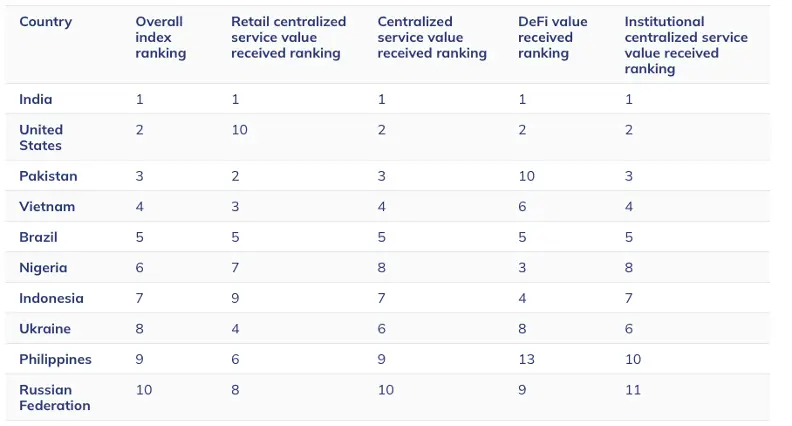

The Chainalysis Global Crypto Adoption Index has ranked India #1 for three consecutive years — 2023, 2024, and 2025. India leads across every sub-index: retail centralised service value, institutional centralised service value, DeFi value received, and overall adoption. The United States ranks second. Pakistan third.

Source: Chainalysis Global Crypto Adoption Index 2025 — India Ranks #1 Across All Categories

This is not a technology adoption curve that India is catching. India is leading it. Yet the paradox is stark: the country with the highest crypto adoption has the least institutional infrastructure to channel that demand into regulated, investor-protected products.

The government has collected Rs 1,095.80 crore in crypto TDS over three years (Rs 221 crore in FY23, Rs 362 crore in FY24, Rs 511 crore in FY25) and issued 44,000 notices to traders who failed to disclose crypto gains, uncovering Rs 888.82 crore in unreported income. The money is already moving. The question is whether it moves through regulated mutual fund structures or continues flowing through unregulated exchanges — including offshore platforms.

The $1.1 Trillion GDP Projection: Breaking Down the CrossTower-USISPF Model

The CrossTower-USISPF report — published in December 2021 in partnership with the US-India Strategic Partnership Forum — projects that the digital asset economy's contribution to India's GDP would grow at 43.1% CAGR, from $5.1 billion in 2021 to $261.8 billion annually by 2032, resulting in a cumulative $1.1 trillion GDP addition over the 11-year period.

The report identifies five primary GDP contribution channels. Government-related blockchain projects alone were estimated to drive $5.1 billion of GDP by 2032, and digital identity applications could contribute $8.2 billion to India's GDP in 2032:

GDP Channel | Estimated 2032 Contribution | How Crypto MFs Accelerate This |

Direct Trading & | $40-60 billion | Regulated MF inflows create stable, recurring volume vs speculative retail trading |

Ancillary Services | $80-120 billion | Every crypto MF needs custodians, NAV calculators, fund auditors — new industry verticals |

Digital Identity & | $8.2 billion (govt est) | MF-grade KYC/AML infrastructure built for crypto benefits all blockchain applications |

Web3 Startups & | $50-80 billion | 450+ Web3 startups get domestic institutional capital instead of relying on offshore VCs |

Tax Revenue & | $15-25 billion | 30% tax on MF crypto gains + GST on services vs current Rs 511 Cr TDS collection |

Source: Grade Capital estimates based on CrossTower-USISPF projections. Government blockchain GDP estimate from the USISPF report.

The Job Creation Multiplier: From 450 Startups to an Industry

According to NASSCOM, India already has over 450 Web3 startups, four unicorns, and 11% of the world's Web3 talent — the third-largest pool globally, growing at 120%+ annually. Over $1.3 billion in Web3 investments have flowed into India since 2020.

But this ecosystem operates under constant regulatory uncertainty. Founders and developers have been relocating to Dubai, Singapore, and EU jurisdictions that offer clearer regulatory frameworks. The brain drain is not hypothetical — it is measurable in the number of Indian-origin Web3 companies now headquartered in the UAE.

A regulated crypto mutual fund framework would reverse this dynamic in several ways. First, institutional capital from AMCs creates a domestic demand floor that does not depend on global VC sentiment. Second, the ancillary services required to support crypto MFs — custody technology, blockchain auditing, NAV calculation engines, compliance automation, and investor education — would create entirely new professional verticals that do not exist in India today. Third, the talent that left would have a reason to return.

Conservative estimates suggest that a functioning crypto MF ecosystem could directly create 50,000-75,000 new jobs within 3-5 years across fund management, custody operations, compliance, technology development, and distribution. The indirect employment multiplier — across legal, accounting, fintech, and education — could be 3-4x that number.

Tax Revenue: From Rs 511 Crore to a Multi-Billion Dollar Stream

India's current crypto tax collection tells the story of untapped potential. The government collected Rs 511.83 crore in crypto TDS in FY25 — on a 1% TDS rate applied to a trading volume of approximately Rs 51,000 crore. This represents a tiny fraction of the $2.36 trillion in total crypto transactions processed through Indian users.

Now model what happens with regulated crypto mutual funds:

Tax Source | Current (FY25) | With Crypto MFs (Est Year 3) | Multiplier |

TDS on Crypto (Sec 194S) | Rs 511 Cr | Rs 2,500-4,000 Cr | 5-8x |

Income Tax on Gains (Sec 115BBH) | Rs 400-600 Cr (est) | Rs 6,000-10,000 Cr | 10-15x |

GST on Fund Mgmt Services | Rs 0 (no funds exist) | Rs 800-1,200 Cr | New stream |

STT Equivalent (if introduced) | Rs 0 | Rs 300-500 Cr | New stream |

Corporate Tax (AMCs, custodians) | Minimal | Rs 1,000-2,000 Cr | New stream |

Estimates assume 2-3% MF AUM allocation, 15% average annual returns on crypto assets, 30% tax rate. Actual outcomes depend on market performance, regulatory structure, and investor participation. These are illustrative projections, not forecasts.

The irony is hard to miss. India taxes crypto at one of the highest rates in the world — 30% flat with no loss offset, no deductions, no carry-forward. But the tax base is narrow because the investment channel is unregulated. Creating regulated crypto Mutual Funds would dramatically expand the tax base while giving investors the protections they currently lack.

Global Competitiveness: What India Risks by Waiting

While India debates, other countries are building. The US approved 11 spot Bitcoin ETFs in January 2024 and accumulated over $114 billion in AUM by November 2025. The EU's MiCA framework is fully operational as of December 2024. Canada, Brazil, Hong Kong, and Australia all have regulated crypto fund products.

The competitive cost of delay is measured in three currencies: capital flight, where Indian investors route money through offshore exchanges and international platforms to access crypto ETFs they cannot buy domestically; talent flight, where developers and founders relocate to crypto-friendly jurisdictions taking their companies, IP, and future tax revenue with them; and innovation flight, where the ancillary infrastructure — custody tech, blockchain analytics, DeFi protocols — gets built elsewhere because India offers no institutional demand anchor.

India's 49 registered crypto exchanges and FIU-IND compliance framework show that the enforcement infrastructure exists. The missing piece is not capability — it is a policy decision to channel existing demand through regulated structures rather than fighting its existence.

What India's First Crypto Mutual Fund Could Look Like

Based on global precedents, India's first crypto MF products would likely follow a phased approach:

Phase 1 would start with passive products — a Bitcoin Index Fund or Crypto Blue-Chip ETF tracking Bitcoin and Ethereum, similar to how India's first equity index funds tracked the Sensex. Low expense ratios, simple structure, institutional custody through licensed digital asset custodians.

Phase 2 would expand to actively managed crypto funds — multi-asset crypto baskets with professional rebalancing, derivatives overlay for risk management, and sector-specific crypto funds (DeFi, Layer-1 infrastructure, stablecoins).

Phase 3 would introduce hybrid products — balanced funds combining equity and crypto exposure (90/10 or 95/5 splits), target-date crypto allocation funds, and crypto SIP products designed for the retail investor who currently puts Rs 3,000/month into equity SIPs.

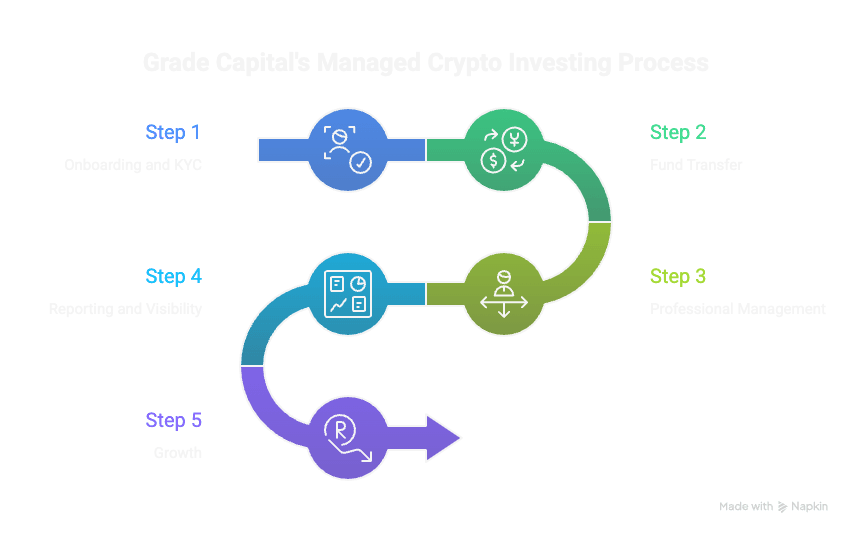

Platforms like Grade Capital already operate in this space — offering managed crypto derivatives portfolios with institutional-grade custody and FIU-IND compliant infrastructure. But these are not mutual funds. The regulatory framework that would allow AMCs like HDFC, ICICI Prudential, or SBI to offer crypto products to their existing 20+ crore folio holders does not yet exist.

The Bottom Line: An Economic Argument, Not a Product Pitch

This is not an argument for reckless deregulation. It is an argument for structured inclusion. India already has the demand, the tax infrastructure (30% VDA tax, 1% TDS, FIU-IND registration), the enforcement capability (49 registered exchanges, 44,000 compliance notices), and the financial literacy (Rs 32,087 crore monthly SIPs). What it lacks is the regulatory bridge that connects this demand to the institutional mutual fund ecosystem.

The economic case is straightforward. A 2-3% MF AUM allocation into regulated crypto funds could generate Rs 10,000-17,000 crore in annual government tax revenue, create 50,000-75,000 direct jobs, reverse the Web3 brain drain, give India's 450+ blockchain startups a domestic institutional capital base, and position the country as a global leader in regulated digital finance — matching its #1 adoption ranking with #1 institutional infrastructure.

The $1.1 trillion GDP projection by 2032 is not a fantasy. It is an economic model built on current growth trajectories. The only variable is whether India chooses to participate in that growth through regulated channels or watches it happen elsewhere.

————————————————————————————————————————

Disclaimer: This content is for informational and educational purposes only and does not constitute financial advice or an offer to invest. All economic projections in this article are estimates based on stated assumptions and publicly available data. They are not forecasts or guarantees. Past performance is not indicative of future results. Tax treatment depends on individual circumstances and the prevailing interpretation of tax laws. Investors are advised to consult with qualified tax professionals to understand how these provisions apply to their specific situation.