What India Needs to Launch Crypto Mutual Funds: A Policy Blueprint for SEBI

India's crypto mutual fund market does not exist — and SEBI's Mutual Funds Regulations 2026 are the reason why. The new regulations, which replaced the 1996 framework on April 1, 2026, overhauled expense ratios, tightened brokerage caps, and modernised NAV calculation norms — yet they left crypto entirely outside the permitted investment universe. The Seventh Schedule, which defines what mutual funds can legally hold, lists equities, debt, gold, silver, InvITs, and REITs. Virtual Digital Assets (VDAs) are absent.

This article is not another explainer on why crypto MFs do not exist in India. That question was answered in our previous piece. This is a practitioner's blueprint: the specific regulatory amendments SEBI would need to make — to custody rules, NAV valuation frameworks, expense structures, and audit standards — to bring crypto into the mutual fund fold. We draw on the US SEC's spot Bitcoin ETF model and the EU's MiCA framework to show what a workable Indian path could look like.

The Seventh Schedule Problem: Why Crypto Cannot Enter MF Portfolios Today

The SEBI (Mutual Funds) Regulations 2026 define the entire operational framework for India's Rs 66 lakh crore mutual fund industry. The Seventh Schedule specifies valuation norms for every permitted asset class: listed equities at closing price, debt instruments at AMFI/CRISIL matrices, gold and silver ETFs at domestic polled spot prices (shifted from LBMA in April 2026), and InvIT/REIT units at exchange-traded prices.

Crypto is not mentioned. Not as a restricted asset. Not as an experimental category. It simply does not exist in the regulatory vocabulary of mutual funds. As former SEBI Chairman Ajay Tyagi stated, SEBI does not want mutual funds to come up with NFOs based on crypto assets until regulations exist. This is the foundational barrier — no AMC can file a scheme information document referencing an asset class that has no valuation norm, no custodial framework, and no risk classification within SEBI's architecture.

The New BER Framework — and the Gap It Reveals

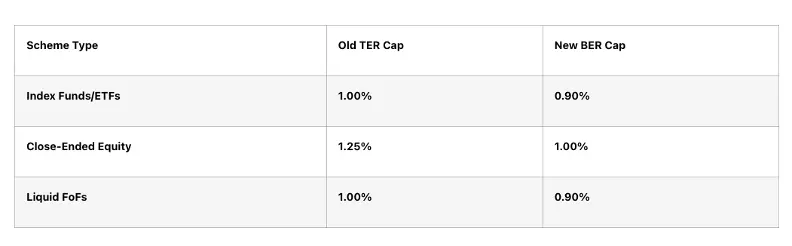

The 2026 Regulations introduced the Base Expense Ratio (BER) framework, replacing the old Total Expense Ratio (TER) caps. BER separates fund management costs from distribution commissions, giving investors clearer visibility into what they pay for portfolio management versus what goes to distributors.

Fig 1: SEBI BER vs Old TER Caps — Key Scheme Types | Source: SEBI MF Regulations 2026, Legallands

The expense reduction is meaningful — Index Funds and ETFs dropped from 1.00% to 0.90%, close-ended equity from 1.25% to 1.00%. Brokerage caps were also tightened: cash market brokerage fell from 12 basis points to 6 bps, and derivatives from 5 bps to 2 bps.

But here is what matters for this discussion: every BER cap applies only to existing permitted asset classes. A hypothetical crypto mutual fund would need its own expense structure — one that accounts for significantly higher custody costs (cold storage, MPC wallets, insurance), 24/7 market monitoring, and blockchain transaction fees that have no equivalent in traditional markets.

What SEBI Would Need to Amend: Five Regulatory Building Blocks

Enabling crypto mutual funds in India is not a single-step process. It requires coordinated amendments across at least five areas of the SEBI MF Regulations 2026.

1. Seventh Schedule: Add VDAs to the Permitted Investment Universe

The most fundamental change. SEBI would need to insert a new category in the Seventh Schedule — "Virtual Digital Assets" or "Digital Assets" — with defined subcategories (Layer-1 tokens, stablecoins, utility tokens) and a positive list of approved assets. This mirrors how SEBI currently permits only LBMA-accredited gold and silver in precious metal ETFs — not all gold, but specific qualifying instruments.

A phased approach could start with a restricted list: Bitcoin and Ethereum only (as the US SEC did with spot ETFs), with criteria for adding assets over time based on market capitalisation, liquidity depth, and track record.

2. Qualified Custodian Framework for Digital Assets

Current SEBI MF custody rules require assets to be held by a SEBI-registered custodian — typically banks or specialised entities like HDFC Bank Custodial Services or Deutsche Bank. These custodians have no infrastructure for crypto custody. A new framework would need to define:

Requirement | Current MF Norm | Proposed Crypto MF Norm |

Custodian Type | SEBI-registered bank/custodian | Licensed digital asset custodian (new category) |

Storage | Demat accounts via CDSL/NSDL | 80%+ cold storage, MPC wallet technology |

Insurance | Standard banking insurance | Crypto-specific theft/hack coverage (A-rated carriers) |

Segregation | Beneficial owner model | On-chain segregation, no rehypothecation |

Audit | Statutory audit + SEBI inspection | On-chain proof-of-reserves + independent crypto audit |

Key Management | N/A (centralised demat) | Multi-party computation (MPC), geographically distributed |

Source: SEBI MF Regulations 2026 (custody provisions), Coinbase Custody Trust Company, Fireblocks architecture

3. NAV Valuation Norms for 24/7 Markets

This is one of the most technically complex challenges. Indian mutual funds calculate NAV at a single point: 3:30 PM IST, when equity markets close. The Seventh Schedule's valuation norms are built around closing prices from recognised exchanges (BSE/NSE) or AMFI-published matrices for debt instruments.

Crypto markets never close. Bitcoin trades 24 hours a day, 365 days a year, across dozens of global exchanges with varying liquidity. A crypto MF NAV framework would need to address:

Cut-off time standardisation: Fix a daily NAV snapshot (e.g., 11:59 PM IST) across all crypto MF schemes. Price source: Use a volume-weighted average price (VWAP) from multiple qualifying exchanges — similar to how the CME CF Bitcoin Reference Rate works for US ETFs. Stale price handling: Define rules for assets with thin liquidity or exchange outages, including fair value adjustments reviewed by the fund's valuation committee. The Seventh Schedule would need a new sub-section dedicated to digital asset valuation, separate from equity, debt, and commodity norms.

4. Expense Ratio Structure for Crypto Schemes

Crypto fund management is structurally more expensive than traditional equity or debt management. Custody alone can cost 25-50 basis points (versus near-zero for demat custody). Blockchain transaction fees (gas fees on Ethereum, for example) are variable and unpredictable. A dedicated BER cap for crypto schemes — potentially higher than equity funds but with clear breakdowns — would be necessary.

A reasonable starting point could be 2.50-3.00% BER for actively managed crypto schemes and 1.25-1.50% for passive crypto index/ETF products, with mandatory disclosure of on-chain transaction costs as a separate line item.

5. Risk Classification and Investor Suitability

SEBI's product labelling norms (the "riskometer") currently range from "Low" to "Very High." Crypto would likely need a new category — possibly "Extremely High" or a dedicated digital asset risk label — with mandatory investor suitability checks, minimum investment thresholds, and concentration limits (e.g., no more than 5-10% of a diversified MF portfolio in VDAs).

How the US Did It: The Spot Bitcoin ETF Custody Model

On January 10, 2024, the US SEC approved 11 spot Bitcoin ETFs simultaneously — including products from BlackRock (IBIT), Fidelity (FBTC), Ark/21Shares (ARKB), and Invesco (BTCO). The approval resolved a decade-long regulatory standoff and established the custody framework that India could study.

The custody architecture centres on Coinbase Custody Trust Company LLC, which serves as the qualified custodian for 8 of the 11 approved ETFs. Coinbase operates as a New York-chartered limited purpose trust company, regulated by the New York Department of Financial Services (NYDFS). Key provisions include segregated client assets with no commingling, prohibition on rehypothecation (the custodian cannot lend or pledge client Bitcoin), cold storage for the vast majority of assets with MPC technology for key management, and SOC 2 Type II and SOC 1 Type II audit certifications.

The BlackRock iShares Bitcoin Trust (IBIT) accumulated over $50 billion in AUM within its first year — making it the fastest-growing ETF in US history. This demonstrated that institutional custody infrastructure can work at scale when the regulatory framework is clear.

For India, the lesson is not to copy the US model directly but to adapt its principles: require licensed, audited custodians with crypto-specific expertise, mandate asset segregation and cold storage minimums, and create a regulatory pathway for entities like Fireblocks or emerging Indian custodians to obtain SEBI licensing.

Fig 2: Crypto Regulation in India — Why SEBI Is Set to Step In | Source: Policy Circle, January 14, 2026

The EU MiCA Precedent: A 36-Month Roadmap India Could Adapt

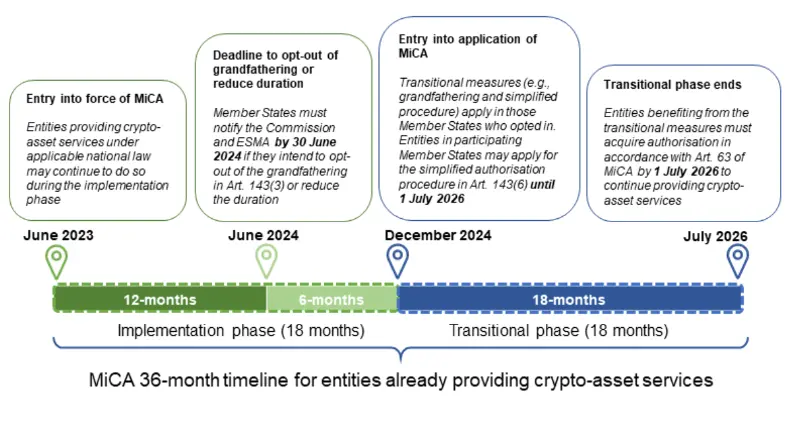

The EU's Markets in Crypto-Assets Regulation (MiCA) is the most comprehensive crypto regulatory framework enacted by any major economy. Regulation 2023/1114 entered into force in June 2023, with full application by December 2024 and a transitional period for existing operators ending July 2026 — a 36-month phased timeline.

MiCA's CASP (Crypto-Asset Service Provider) authorization framework is directly relevant to the custody question for Indian crypto MFs. Key requirements include minimum capital reserves of EUR 50,000 to EUR 150,000 depending on service type, mandatory client asset segregation from the firm's own assets, explicit hot wallet and cold wallet governance policies, cyber resilience testing and incident reporting, and professional indemnity insurance or equivalent own funds.

Fig 3: MiCA 36-Month Timeline for Existing Crypto-Asset Service Providers | Source: ESMA

The ESMA technical standards for MiCA cover everything from disclosure requirements for crypto-asset white papers to market abuse surveillance for crypto trading venues. India's SEBI would need equivalent technical standards — not just a high-level framework but detailed operational rules that AMCs, custodians, and auditors can implement.

The MiCA timeline is instructive. Even with the EU's institutional capacity, it took 36 months from entry into force to full compliance. India, starting from a position of no existing crypto law, would realistically need 24-36 months from legislation to the first crypto Mutual Fund NFO — assuming political will exists.

A Practical Roadmap: From Current State to First Crypto MF NFO

Based on the US and EU precedents, and the specific architecture of SEBI MF Regulations 2026, a realistic path to India's first crypto mutual fund would involve the following phases:

Phase | Timeline | Key Actions | Dependencies |

Phase 1: | Months 1-12 | Parliament passes dedicated crypto/VDA law | Political consensus |

Phase 2: | Months 6-18 | Seventh Schedule amendment (add VDAs) | Crypto law enacted |

Phase 3: | Months 12-24 | Custodians apply for SEBI licensing | SEBI framework published |

Phase 4: | Months 18-30 | AMCs file crypto MF scheme documents | All infrastructure ready |

Note: Phases overlap. Total estimated timeline: 24-30 months from legislation to first NFO.

What This Means for Indian Investors Today

The blueprint above is not aspirational thinking. Every element — custody licensing, NAV methodology, expense structures, phased implementation — has been executed in at least one major jurisdiction. The US did it for spot ETFs. The EU did it comprehensively through MiCA. Canada, Australia, Brazil, and Hong Kong have their own versions.

India's regulatory apparatus has the technical capability. SEBI's 2026 Regulations demonstrate sophisticated thinking on expense structures, valuation methodology, and investor protection. The shift from LBMA to domestic polled prices for gold/silver ETFs shows SEBI can adapt valuation norms when the asset class demands it.

The missing ingredient is not regulatory capacity — it is a dedicated crypto law that gives SEBI the legal mandate to act. Until that law exists, the Seventh Schedule cannot be amended, custody norms cannot be drafted, and no AMC can file a crypto MF scheme.

In the interim, Indian investors seeking professionally managed crypto exposure have limited options. Platforms like Grade Capital offer managed crypto derivatives portfolios that operate within the existing regulatory framework — using futures and options rather than spot crypto holdings, with institutional-grade custody through Fireblocks and FIU-IND compliant on-ramp partner like Onmeta. These are not mutual funds, but they represent the closest available alternative for investors who want professional crypto portfolio management without waiting for the regulatory framework to materialise.

————————————————————————————————————————

Disclaimer: This content is for informational and educational purposes only and does not constitute financial advice or an offer to invest. Past performance is not indicative of future results. Tax treatment depends on individual circumstances and the prevailing interpretation of tax laws. Investors are advised to consult with qualified tax professionals to understand how these provisions apply to their specific situation.