A crypto mutual fund would let Indian investors gain diversified exposure to digital assets through a SEBI-regulated, NAV-based pooled vehicle, much like an equity or debt mutual fund. The appeal is obvious: professional management, regulatory oversight, and the convenience of SIP-style investing applied to Bitcoin, Ethereum, and other crypto assets. For many retail investors searching for a bitcoin mutual fund or crypto fund India option, the expectation is that such a product should already exist given India's massive crypto adoption.

But as of May 2026, no crypto mutual fund exists in India. Not because the demand is absent, as over 572,000 new crypto SIPs were created on CoinDCX alone in 2025, but because a three-way regulatory deadlock between SEBI, the RBI, and the Finance Ministry has made it structurally impossible for any asset management company to launch one.

This guide explains what a crypto mutual fund is, why India does not have one yet, and the five alternatives Indian investors can use today to gain crypto exposure legally and tax-efficiently. Whether you are searching for a bitcoin mutual fund, a crypto fund India option, or simply want to understand your options, this is a comprehensive analysis of the current landscape.

What Is a Crypto Mutual Fund?

A crypto mutual fund is a pooled investment vehicle that allocates capital across one or more digital assets, offering daily NAV-based pricing, professional portfolio management, and regulatory oversight from a securities authority. Investors buy units, and the fund manager handles custody, rebalancing, and compliance.

Globally, such products already exist. Canada launched the Purpose Bitcoin ETF in February 2021, the first physically backed Bitcoin ETF in North America. In Europe, 21Shares operates a suite of crypto exchange-traded products listed on SIX Swiss Exchange. Brazil has the Hashdex Nasdaq Crypto Index Fund, which tracks a diversified crypto index. And in January 2024, the United States approved 11 spot Bitcoin ETFs, led by BlackRock's iShares Bitcoin Trust (IBIT), which has grown to over $64.7 billion in net assets within 18 months of launch.

In India, however, mutual funds are governed by the SEBI (Mutual Funds) Regulations, 1996, and no classification exists for crypto or virtual digital assets (VDAs) as an eligible underlying asset class.

Why Crypto Mutual Funds Don't Exist in India Yet

The absence of a crypto mutual fund in India is not due to a lack of investor appetite. It is the result of a sustained regulatory impasse involving three institutions, each with a different stance on cryptocurrency.

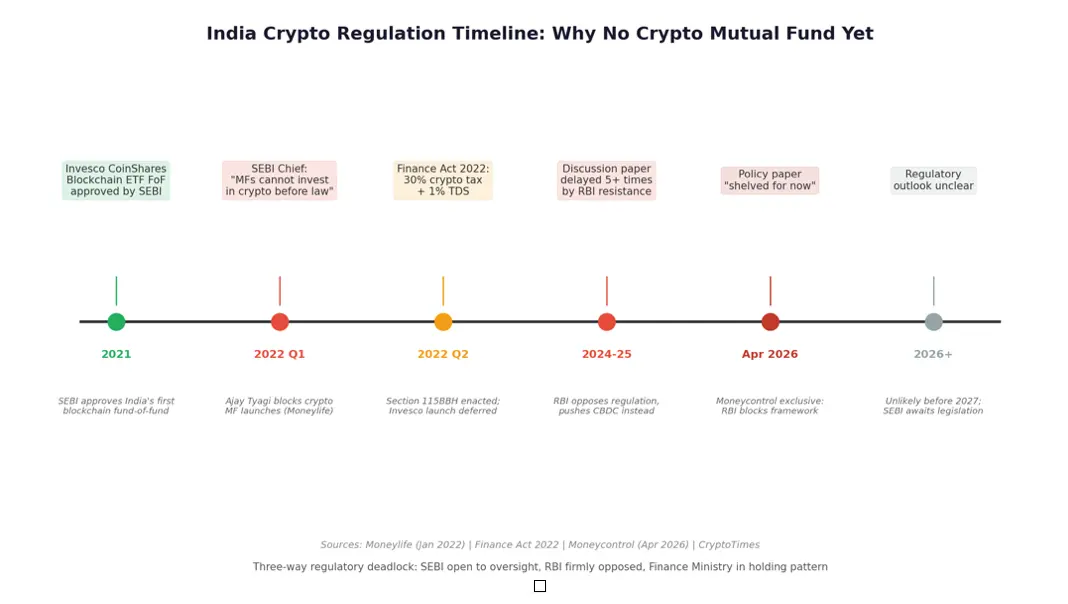

SEBI has signalled openness to oversight. Former chairperson Madhabi Puri Buch acknowledged that crypto regulation could fall under its purview if assets were classified as securities. Current chairman Tuhin Kanta Pandey has taken a more cautious position, stating clearly that mutual funds cannot make crypto-related investments until the government enacts specific legislation. This position was first articulated by former SEBI chief Ajay Tyagi in early 2022, when he said SEBI does not want mutual funds to come up with new fund offers based on crypto assets until the government has announced regulations for cryptocurrencies.

Figure 1: India Crypto Regulation Timeline (Sources: Moneylife, Moneycontrol, Finance Act 2022)

The Reserve Bank of India has been the most vocal opponent. The RBI has consistently argued that cryptocurrencies pose systemic risks to financial stability and has advocated for an outright ban. Since July 2024, the Finance Ministry's cryptocurrency discussion paper, which was expected to provide a regulatory framework, has been delayed at least five times, primarily due to RBI objections. In April 2026, Moneycontrol reported that the policy paper has been shelved for now as the government relies on taxation and FIU-led monitoring rather than a dedicated regulatory framework.

The Finance Ministry occupies the middle ground. While it introduced a 30% flat tax on crypto gains (Section 115BBH) and 1% TDS on transactions via the Finance Act 2022, it has not tabled any legislation to regulate or recognize cryptocurrencies as a distinct asset class. Without such legislation, SEBI lacks the legal authority to approve crypto-linked mutual fund schemes.

The Closest India Got: Invesco CoinShares Global Blockchain ETF Fund-of-Fund

In 2021, Invesco Mutual Fund received SEBI approval to launch the Invesco CoinShares Global Blockchain ETF Fund-of-Fund (FoF), making it the first blockchain-linked scheme to get regulatory clearance in India. The parent fund, listed on the London Stock Exchange, tracks the CoinShares Blockchain Global Equity Index, which invests in companies participating in the blockchain ecosystem rather than holding crypto directly.

The NFO was originally scheduled to open for subscription on November 24, 2021. However, the launch was deferred indefinitely following the SEBI chief's statement that mutual funds should not pursue crypto-linked NFOs until regulatory clarity emerges. As of May 2026, the scheme remains approved on paper but has never opened to investors, making it a case study in how India's regulatory gridlock has frozen even indirect blockchain exposure through traditional mutual fund channels.

5 Alternatives Indian Investors Can Use Today

While a crypto mutual fund remains unavailable, Indian investors have several legal pathways to gain crypto exposure. Each comes with its own risk profile, tax treatment, and regulatory standing.

Alternative 1: Crypto SIP on Indian Exchanges

The most accessible option for retail investors. Platforms like CoinDCX, CoinSwitch, and WazirX offer automated crypto SIP plans starting at as little as Rs 100 per month. Investors choose a token (Bitcoin, Ethereum, or others), set a frequency (daily, weekly, or monthly), and the platform auto-debits and purchases at prevailing market prices.

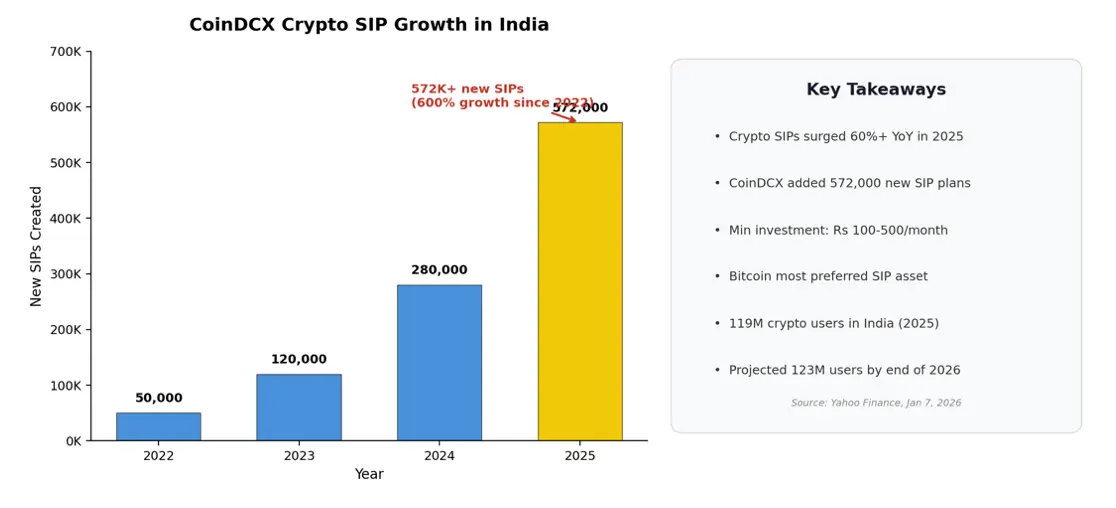

Figure 2: India Crypto SIP Growth (Source: Yahoo Finance, CoinDCX data, Jan 2026)

The growth has been significant: CoinDCX reported over 572,000 new SIP plans created in 2025 alone, representing a 600% year-over-year surge since the feature launched in 2022. The average monthly SIP amount starts at just Rs 100, making it the lowest-barrier entry point into crypto. India now leads global crypto adoption with 119 million users in 2025, projected to reach 123 million by end of 2026.

Tax treatment: All gains are taxed at a flat 30% under Section 115BBH, with 1% TDS deducted on every transaction. No deductions or set-offs are allowed against other income or losses.

Alternative 2: Blockchain ETF Fund-of-Funds

If the Invesco CoinShares Global Blockchain ETF FoF eventually launches, it would offer indirect blockchain exposure through equity holdings in companies like Coinbase, MicroStrategy, and other blockchain ecosystem participants. This is not a direct crypto investment, as the parent fund holds equity shares, not tokens.

The tax advantage is meaningful: as an equity-oriented mutual fund, it would attract 12.5% LTCG on gains above Rs 1.25 lakh after a one-year holding period, significantly lower than the flat 30% VDA tax. However, given the launch has been pending for over four years, investors should treat this as a future possibility rather than a current option.

Alternative 3: US Bitcoin ETFs via the LRS Route

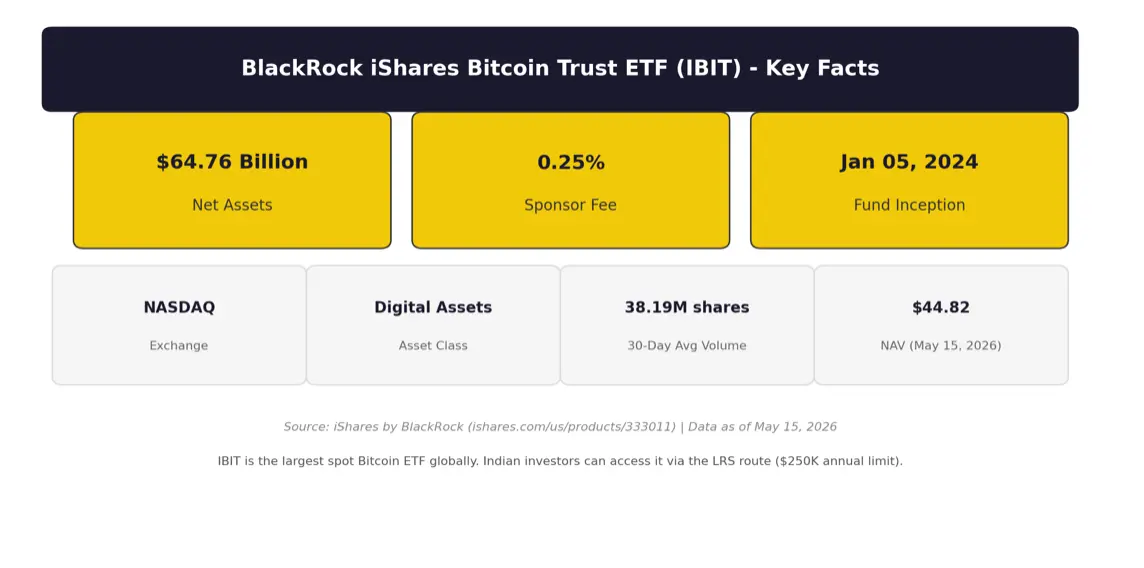

Indian residents can invest in US-listed spot Bitcoin ETFs through the Liberalised Remittance Scheme, which allows up to $250,000 in outward remittance per financial year. The most prominent option is BlackRock's iShares Bitcoin Trust (IBIT), the world's largest spot Bitcoin ETF with over $64.7 billion in net assets, a 0.25% sponsor fee, and daily trading volume exceeding 38 million shares.

Figure 3: BlackRock IBIT Key Facts (Source: iShares by BlackRock, May 2026)

The critical tax advantage: US Bitcoin ETFs acquired via LRS are classified as foreign assets, not as Virtual Digital Assets under Indian tax law. This means they attract 12.5% LTCG after a 24-month holding period, not the 30% flat tax that applies to direct crypto. The difference is substantial, and for long-term investors, this remains the most tax-efficient route to Bitcoin exposure from India.

Costs to consider: A 20% Tax Collected at Source applies on LRS remittances exceeding Rs 10 lakh per financial year (adjustable against final tax liability), and brokerage charges for US stock accounts apply. Important caveat: In September 2025, IFSCA restricted access to crypto ETFs for Indian residents investing through GIFT City via Clause 20 of the revised Global Access Circular. Direct LRS investments through international brokers remain unaffected by this restriction.

Alternative 4: Managed Crypto Portfolios

For investors seeking a more structured, hands-off approach, managed crypto portfolio platforms like offer algorithm-driven, diversified portfolio management. These are not pooled funds or mutual funds; instead, each investor maintains a separate account with direct ownership of the underlying assets, while the platform handles allocation, rebalancing, and risk management. Grade Capital is one and only example of this model in India.

This model offers the professional management element that a crypto mutual fund would provide, without the pooled-fund structure that requires SEBI approval. The tax treatment follows VDA rules: 30% flat tax under Section 115BBH, with 1% TDS on transactions. But Grade Capital deals in Managed derivatives (futures + options) so the tax structure is treated under Slab rates as speculative business income.

Alternative 5: Crypto Baskets and Index Products

Several Indian platforms offer pre-built thematic baskets, such as a DeFi basket, Layer-1 basket, or Top-10 basket, that bundle multiple tokens into a single investment. Unlike a mutual fund, these are not NAV-based pooled vehicles. The investor directly owns the underlying tokens, and prices reflect real-time market rates rather than end-of-day NAV.

The advantage is diversification without manual selection. The limitation is that these products lack the regulatory framework, disclosure requirements, and investor protections that come with a SEBI-regulated mutual fund. Tax treatment is the same as direct crypto: 30% flat under Section 115BBH.

Tax Comparison: Which Route Is Most Efficient?

Route | Tax Rate | TDS / TCS | LTCG Holding Period | Key Section |

Direct Crypto (SIP) | 30% flat | 1% TDS | N/A (flat rate) | Sec 115BBH |

Blockchain ETF FoF | 12.5% LTCG | None | 1 year | Equity MF rules |

US Bitcoin ETF (LRS) | 12.5% LTCG | 20% TCS > Rs 10L | 24 months | Foreign asset |

Managed Portfolio |

| 1% TDS | N/A (flat rate) | Section 43(5) and Section 73 |

Crypto Baskets | 30% flat | 1% TDS | N/A (flat rate) | Sec 115BBH |

The LRS route stands out as the most tax-efficient option for long-term Bitcoin exposure, with a potential tax saving of 17.5 percentage points (12.5% vs 30%) compared to direct crypto. However, it requires navigating international brokerage accounts, currency conversion, and the $250,000 annual LRS limit.

What Could Change: Regulatory Outlook

The path to a crypto mutual fund in India depends on legislative action. SEBI has made clear that it will not authorize crypto-linked fund schemes without a statutory mandate. The most likely scenarios are:

First, the Finance Ministry could table a Cryptocurrency Regulation Bill that classifies VDAs as a recognized asset class and designates SEBI as the regulator. This would immediately open the door for crypto mutual funds, ETFs, and other regulated products. However, with the RBI's sustained opposition and no bill currently in the pipeline, this appears unlikely before 2027 at the earliest.

Second, India could adopt elements of the IMF-FSB Global Crypto-Asset Regulatory Framework, which India co-championed during its G20 presidency in 2023. This framework recommends that jurisdictions apply existing financial regulations to crypto activities proportional to the risks they pose. A phased implementation could begin with institutional products before extending to retail mutual fund schemes.

Third, market pressure could force incremental regulatory accommodations, as it did with the introduction of the 30% tax in 2022. If crypto adoption continues growing at the current pace (119 million users in 2025, projected 123 million by end of 2026), the government may find it increasingly difficult to justify the absence of a regulated investment framework.

Until then, the search for a crypto mutual fund in India will remain unfulfilled. Investors searching for a bitcoin mutual fund or a crypto fund India option should focus on the five alternatives outlined above, each of which provides a legitimate pathway to digital asset exposure within the current regulatory and tax framework. The key is to evaluate each route based on individual investment goals, time horizon, tax bracket, and risk tolerance rather than waiting for a product that may not arrive for years.

For context, even in markets where crypto regulation is more advanced, the evolution from first-generation products to diversified crypto mutual funds took several years. The US approved single-asset spot Bitcoin ETFs in January 2024 but has not yet approved a diversified crypto index mutual fund. India's eventual regulatory framework, whenever it arrives, is likely to follow a similarly phased approach, with single-asset exposure preceding multi-asset crypto funds.

Disclaimers

Performance Disclaimer: Past performance of any investment, including cryptocurrencies and crypto-related products, is not indicative of future results. Returns can vary significantly, and investors may lose part or all of their capital.

Tax Disclaimer: Tax information presented in this article is based on the Income Tax Act as applicable in FY 2025-26 and is provided for general informational purposes only. Tax laws are subject to change. Consult a qualified tax advisor before making investment decisions based on tax considerations.

General Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or legal advice. Grade Capital is not a mutual fund and does not operate a pooled investment vehicle. Cryptocurrency investments are subject to market risks, regulatory risks, and technological risks. Always conduct your own research and consult qualified professionals before investing.