Managed Crypto Investment vs Buying Crypto Yourself: What's Right for Indian Investors

Managed crypto investment exists because most people lose money doing it themselves. The Bank for International Settlements — the central bank of central banks — published Bulletin 69 covering crypto investor outcomes across 95 countries between 2015 and 2022. The finding: 73 to 81% of retail crypto investors lost money.

The majority bought during price rallies and sold during crashes — the precise opposite of what generates returns. This is not a reflection on crypto as an asset class. It is a reflection on how most people interact with it.

The distinction between managed crypto investment and self-directed buying is, at its core, the distinction between structured exposure and unstructured exposure to the same underlying market.

The Reality of Self-Directed Crypto Investing

A JPMorgan Chase Institute study reinforces the BIS data — tracking crypto investor behaviour across multiple market cycles. The median retail investor experienced negative returns. Lower-income households bought at substantially higher prices than wealthier ones.

The pattern is consistent across geographies and timeframes. Retail investors drive sell-offs during downturns. Large holders — institutional investors and high-net-worth individuals — sell before declines and accumulate during drawdowns. The BIS study categorised these two groups as "whales" and "krill." The metaphor is precise.

A separate study from the University of São Paulo tracked 19,646 day traders over a multi-year period. 97% of those who persisted beyond 300 days lost money. The median day trader earned less than minimum wage. Only 1.1% earned more than Brazil's minimum wage from trading.

In India, the challenge compounds. The crypto market operates 24/7 across global time zones. Price-moving events occur during US and European trading hours — often while Indian retail investors are asleep.

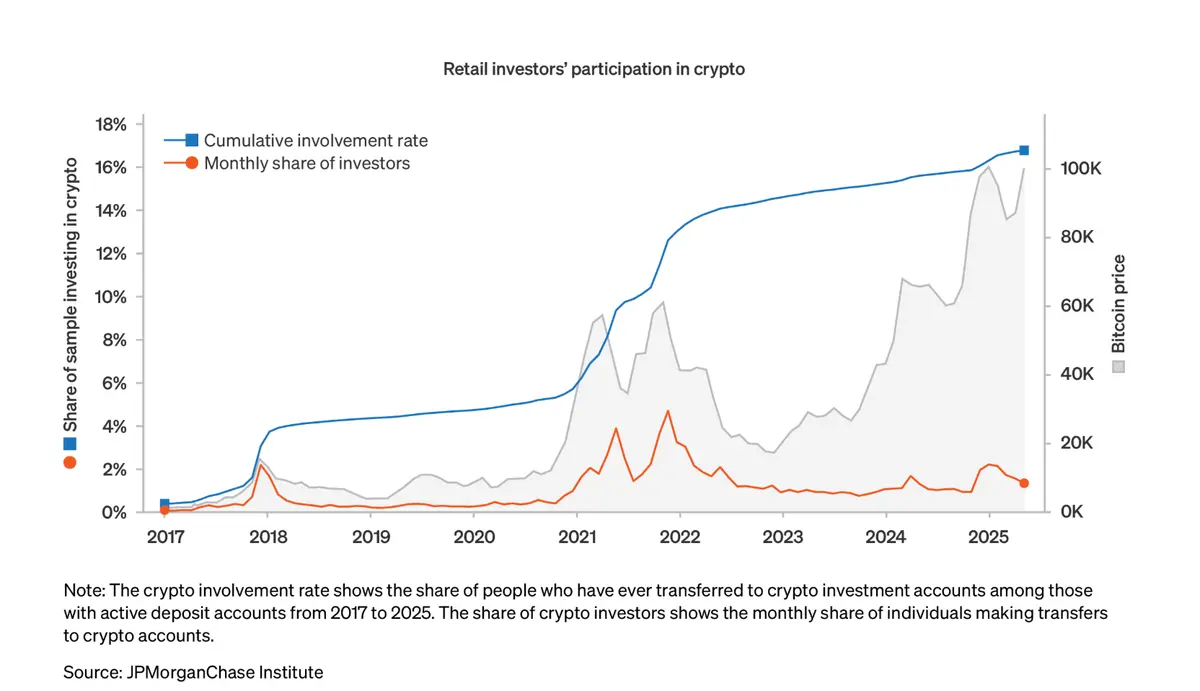

Self-directed investors face an informational and temporal disadvantage that no amount of chart-reading can overcome. India has over 19 million crypto investors — 75% of them under 35, and 40% from Tier-2 and Tier-3 cities. The demographic is young, growing, and largely without access to professional portfolio management. The result is a market where retail capital enters at the worst possible moments and exits too late.

How Managed Crypto Investment Works

Managed crypto investment is not a savings account. It is an active portfolio strategy — typically run by professional fund managers — that uses instruments beyond spot buying to generate returns and control risk.

The most common structure involves three components: spot positions in established digital assets, derivatives (futures and options) for hedging and directional bets, and systematic rebalancing based on quantitative models. The derivatives component is what separates managed exposure from simply buying and holding.

A 2024 study by Vojtko and Dujava, published on SSRN through QuantPedia, tested this distinction directly. A cold storage portfolio — passive buy-and-hold — delivered 57% annualised returns. Impressive on paper. But it carried 67% annualised volatility and a maximum drawdown of -77%.

The same study tested hedged strategies using derivatives overlays. The results: 44 to 47% annualised returns with 34 to 43% volatility — roughly half the risk. Maximum drawdown dropped to -22% to -37%.

The implication is direct. A managed crypto investment strategy using derivatives preserved 77 to 82% of the raw return while cutting volatility by half and reducing the worst-case drawdown by a factor of two to three. The investor who held passively through a -77% drawdown needed a 335% recovery to break even. The hedged investor, at -22%, needed only a 28% recovery.

These are not marginal differences. They represent fundamentally different risk-return profiles from the same underlying asset class — separated only by the presence or absence of professional risk management.

Managed Crypto Investment vs DIY: A Direct Comparison

The differences are structural, not cosmetic.

Parameter | DIY Crypto Investing | Managed Crypto Investment |

|---|---|---|

Strategy | Spot buying/selling based on personal judgement | Derivatives hedging, systematic rebalancing, quantitative models |

Returns (annualised) | Median retail investor: negative (JPMorgan) | Hedged strategies: 44-47% (QuantPedia/SSRN) |

Volatility | 67% for passive hold (QuantPedia) | 34-43% for hedged strategies (QuantPedia) |

Max drawdown | -77% (QuantPedia) | -22% to -37% (QuantPedia) |

Risk management | Manual stop-losses, often overridden by emotion | Systematic hedging via futures and options |

Time commitment | 24/7 market monitoring required | Delegated to fund managers |

Tax (India — spot) | 30% flat, no loss offset (Section 115BBH) | 30% flat, no loss offset (Section 115BBH) |

Tax (India — derivatives) | Slab rate under Section 43(5) | Slab rate under Section 43(5) |

Transparency | Portfolio-level tracking by investor | Daily NAV, audited reporting |

Behavioural risk | High — FOMO, overtrading, anchoring | Eliminated from investment decisions |

Institutional adoption | N/A | 47% of traditional hedge funds now have digital asset exposure (PwC/AIMA) |

The tax treatment is identical for spot positions. The structural difference lies in risk-adjusted returns — and specifically in how derivatives usage compresses the volatility envelope while preserving a significant portion of upside.

The Sharpe ratio — the standard measure of risk-adjusted return — illustrates this clearly. A passive crypto portfolio with 57% return and 67% volatility produces a Sharpe ratio below 0.85. A hedged managed crypto investment strategy with 47% return and 34% volatility produces a Sharpe ratio above 1.38. In portfolio theory, anything above 1.0 is considered strong. The managed approach delivers nearly double the risk-adjusted performance of buying and holding the same assets.

The Behavioural Gap in Crypto Markets

Raw returns are one variable. Investor behaviour is another — and in crypto, the second variable often dominates the first.

The behavioural finance literature identifies four primary biases that affect crypto investors disproportionately. FOMO — fear of missing out — drives buying at cycle peaks, precisely when risk is highest. Overtrading generates transaction costs and tax events without improving outcomes.

Confirmation bias leads investors to seek information that validates existing positions rather than challenging them. Anchoring causes investors to hold losing positions past rational exit points because they are fixated on a previous high.

These biases carry real, measurable costs. The BIS data quantifies their cost: the majority of retail investors bought during price rallies and sold during crashes. The JPMorgan data confirms it: lower-income households — typically newer to investing and more susceptible to hype cycles — consistently entered at higher prices.

Managed crypto investment removes the investor from the decision loop. Fund managers execute allocation, hedging, rebalancing, and exit decisions systematically — based on quantitative signals, not emotional responses.

This is not a guarantee of positive returns. It is the elimination of a documented source of negative ones.

The scale of this behavioural drag is significant. A retail investor who bought Bitcoin at the November 2021 peak of $69,000 and panic-sold at the June 2022 low of $17,600 realised a -74% loss. A managed fund with derivatives hedging — based on the QuantPedia parameters — would have contained that drawdown to -22% to -37%, preserving both capital and the ability to participate in subsequent recovery.

The Institutional Shift Toward Managed Crypto Investment in India

The institutional shift is already measurable. The PwC/AIMA 6th Annual Global Crypto Hedge Fund Report — published in October 2024 — documents the trend in detail.

47% of traditional hedge funds now have digital asset exposure. Derivatives usage among crypto-focused funds rose to 58%, up from 38% in the prior survey. Spot-only trading dropped to 25%.

Market-neutral strategies — which profit from hedging and relative value rather than directional bets — account for 33% of fund strategies.

43% of funds report increased institutional interest from pension funds, family offices, and sovereign wealth entities. The direction is clear: the capital entering crypto markets is increasingly choosing managed, hedged, derivatives-based exposure over direct spot buying. The smart money is not buying Bitcoin on an exchange app.

In India, this shift is nascent but accelerating. The 19 million crypto investors in the country represent a growing pool of capital — most of it managed individually, without derivatives hedging or systematic risk controls.

The gap between available capital and available expertise is where managed crypto investment operates. A professionally managed portfolio with daily NAV tracking, derivatives-based risk management, and transparent reporting addresses the structural disadvantages that self-directed investors face.

The tax framework adds another layer. Spot crypto gains attract 30% flat tax under Section 115BBH with no loss offset — meaning investors pay tax on winning trades even when their portfolio is net negative. Derivatives income under managed portfolios falls under Section 43(5) at slab rates, with loss offset permitted against other speculative income.

Evaluation Criteria for a Managed Crypto Investment Portfolio

Not all managed exposure is equivalent. The difference between a well-structured crypto fund and a poorly constructed one is as significant as the difference between managed and self-directed investing.

Five parameters distinguish credible managed crypto investment portfolios. First: strategy transparency — the fund discloses whether it uses spot, derivatives, or a combination, and the general logic of its hedging approach.

Second: daily NAV reporting — crypto markets move too fast for monthly or quarterly valuations to be meaningful. Third: drawdown history — a fund that has navigated at least one full market cycle (peak to trough to recovery) demonstrates its risk management under real conditions.

Fourth: tax structure clarity — investors know upfront how gains classify under Indian law, whether as spot VDA income under Section 115BBH (30% flat) or as derivatives income under Section 43(5) (slab rates). Fifth: minimum investment and accessibility.

Institutional-quality managed crypto investment has historically required large minimums. Funds that offer lower entry points — such as Grade Capital's ₹ 12,000 minimum with daily NAV tracking and derivatives-based strategies — broaden access to a model previously available only to high-net-worth investors.

The Bottom Line

Crypto's investment potential is not in dispute — the asset class has delivered returns unmatched by any traditional market over the past decade. The real variable is how that exposure is structured. The data on managed crypto investment versus self-directed buying leaves little room for ambiguity.

73 to 81% of retail investors lose money doing it themselves. Hedged, derivatives-based managed crypto investment strategies have historically delivered 44 to 47% annualised returns at half the volatility.

The institutional world has already made its choice — 58% derivatives usage, 25% spot-only, and rising. For Indian investors, the decision framework reduces to a single honest assessment: evaluate your own capacity for 24/7 market monitoring, derivatives knowledge, and emotional discipline under -77% drawdowns.

If that capacity exists, self-directed investing is viable. For most, the data points toward managed crypto investment as the more rational path.

Explore how managed crypto portfolios bring structure and risk management to crypto investing at https://grade.capital