Value averaging vs DCA in crypto is not a theoretical debate. Backtested data across Bitcoin's entire price history shows that value averaging — a strategy that adjusts each instalment based on portfolio performance — outperformed fixed-amount dollar cost averaging in every single year from 2010 to 2019. The difference: approximately 20% higher returns over a decade, with the same underlying asset and the same commitment to systematic investing.

Yet almost every crypto SIP product in India today uses only fixed-amount DCA. CoinDCX created over 572,000 new SIPs in 2025. CoinSwitch saw 59% growth. Mudrex recorded a 220% surge. All of them offer the same thing: invest a fixed rupee amount at regular intervals. None offer value averaging.

This article examines why that gap exists, what the research says about both strategies, and whether value averaging belongs in a serious crypto investor's toolkit.

What Is Dollar Cost Averaging (Fixed Amount DCA)?

Dollar cost averaging is a systematic investment strategy where you invest a fixed amount at regular intervals — weekly, fortnightly, or monthly — regardless of the asset's price. If you commit ₹1,000 per month to Bitcoin, you invest exactly ₹1,000 whether Bitcoin is at ₹45 lakh or ₹75 lakh.

The mathematical result is straightforward. Your average cost converges toward the harmonic mean of prices over time — always lower than or equal to the arithmetic mean. When prices are low, your fixed amount buys more units. When prices are high, it buys fewer. Over time, this naturally accumulates more units at lower prices.

In India, this is what every "crypto SIP" product actually is — a recurring fixed-rupee purchase. The term "SIP" borrows legitimacy from SEBI-regulated mutual fund SIPs, but the underlying mechanism is simply DCA applied to crypto.

What Is Value Averaging? The Strategy DCA Ignores

Value averaging was introduced by Michael Edleson, a Harvard Business School professor and later Managing Director at Morgan Stanley, in a 1988 research article. He expanded it into a book, Value Averaging: The Safe and Easy Strategy for Higher Investment Returns (Wiley, 1993).

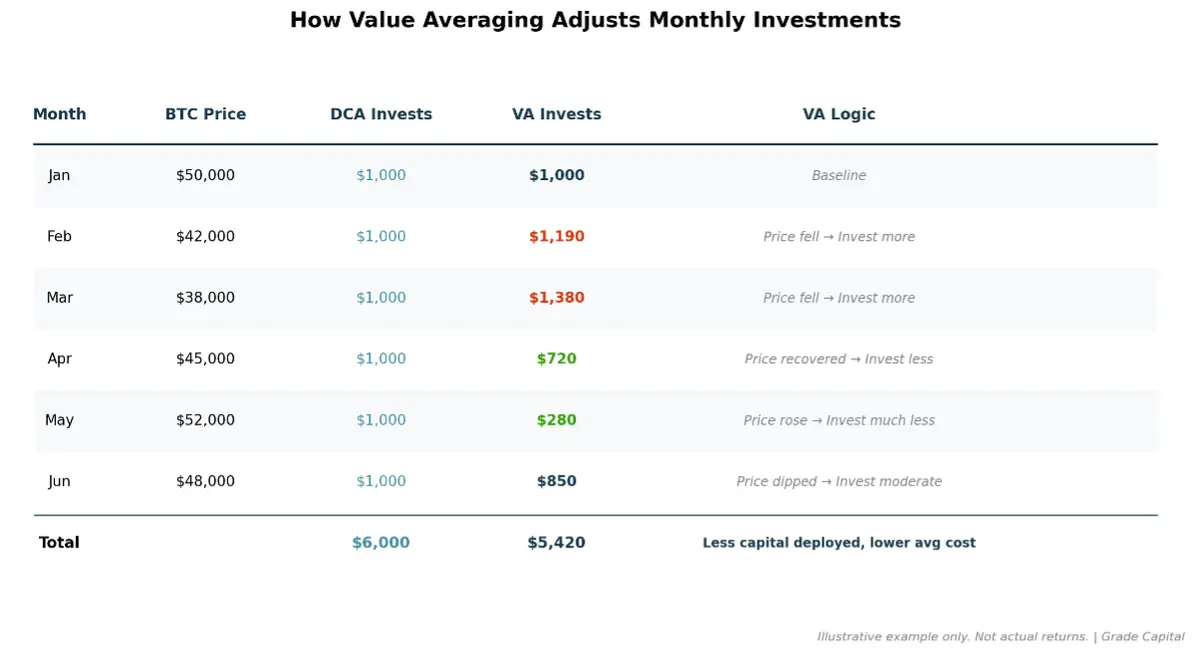

The core idea: instead of investing a fixed amount each period, you set a target portfolio value (a "value path") and invest whatever amount is needed to bring your portfolio back to that target.

If your target says your portfolio should be worth ₹2,000 by Month 2, and after Month 1's investment your portfolio has fallen to ₹850 due to a price drop, you invest ₹1,150 in Month 2 (not the standard ₹1,000). Conversely, if your portfolio has risen to ₹1,800 due to a rally, you invest only ₹200.

The formula for the value path, as Edleson defined it:

V(t) = C × t × (1 + r)ᵗ

Where V(t) is the target value at period t, C is the base periodic contribution, and r is the expected growth rate. The investment each period = V(t) minus current portfolio value.

Figure 1: How Value Averaging adjusts monthly investments based on portfolio value vs target. Illustrative example only.

What the Research Says: Value Averaging vs DCA in Crypto

Three rigorous sources provide the evidentiary backbone for comparing these strategies in crypto markets.

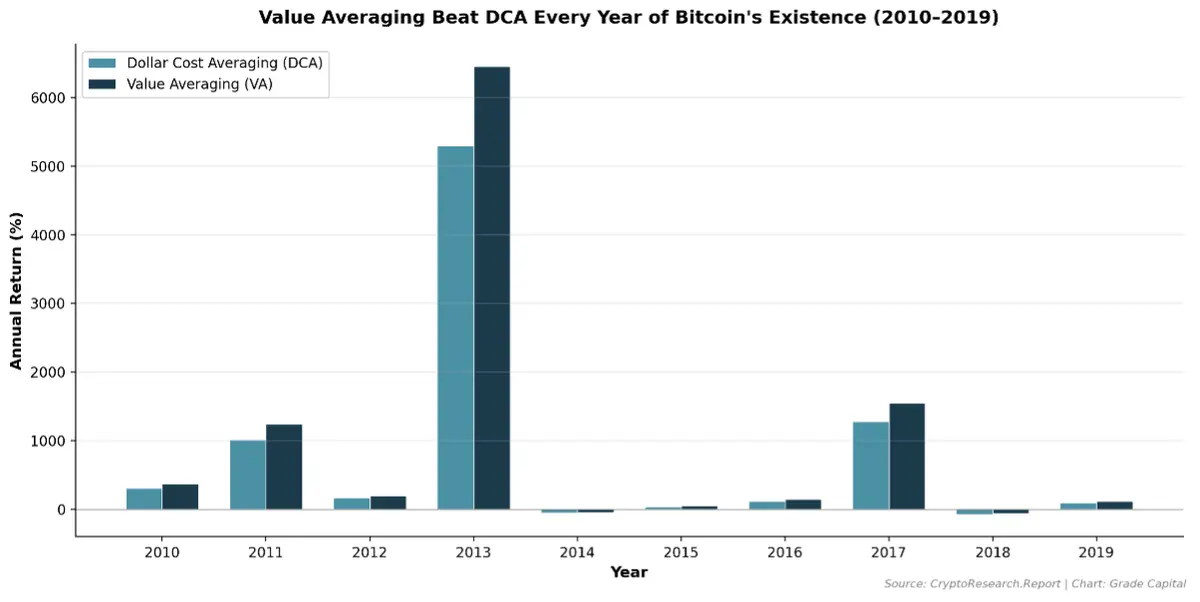

Crypto Research Report (2020): VA Beat DCA Every Year for Bitcoin

Demelza Hays at Crypto Research Report backtested both strategies using CoinMarketCap price data across Bitcoin's entire tradeable history (2010–2019). The findings were unambiguous: value averaging produced higher returns than DCA in all 10 years tested. Over the full decade, VA increased total returns by approximately 20% compared to fixed-amount DCA.

The study compared three strategies — Buy and Hold, Dollar Cost Averaging, and Value Averaging — each deploying $1,000 per year. VA consistently achieved a lower average purchase price by automatically increasing allocation during price declines and reducing allocation during rallies.

Figure 2: Value Averaging beat Dollar Cost Averaging in every year of Bitcoin's existence (2010–2019). Source: Crypto Research Report, CoinMarketCap data.

In a specific 10-month example using real 2019 Bitcoin prices, VA resulted in deploying only $934.49 at an average price of $42,569.95 per BTC, compared to DCA's full $1,000 at an average of $44,787.38. Less capital deployed. Lower average cost. Higher returns.

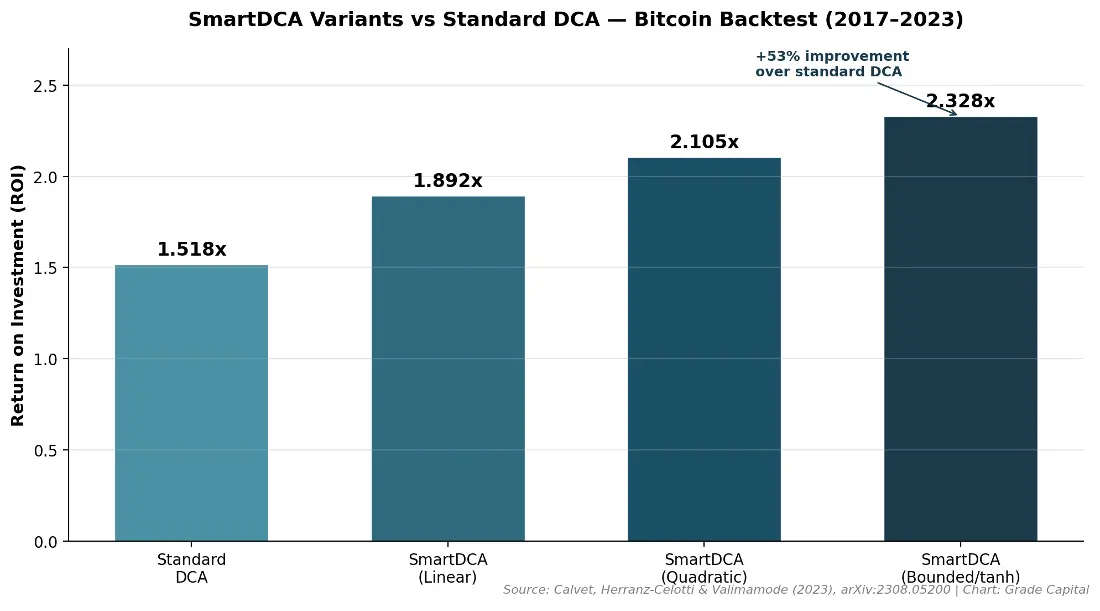

Calvet et al. (2023): SmartDCA — Mathematical Proof of Superiority

Calvet, Herranz-Celotti, and Valimamode (2023) did not merely backtest — they proved mathematically that any DCA variant which adjusts purchase amounts inversely to price will always achieve a lower average cost than fixed-amount DCA. The proof uses the Cauchy–Schwarz inequality and Lehmer means.

Their strategy, called SmartDCA, invests an amount proportional to the inverse of the asset's price. When price is below average, you invest more. When above, you invest less. This is the mathematical formalisation of what value averaging does intuitively.

Backtested on Bitcoin from 2017 to 2023, the bounded SmartDCA variant (using a tanh function to cap maximum investment per period) achieved an ROI of 2.328x versus standard DCA's 1.518x — a 53% improvement with the same underlying asset exposure.

Strategy | ROI (Bitcoin 2017–2023) | Improvement vs DCA |

Standard DCA (Fixed Amount) | 1.518x | Baseline |

SmartDCA (Linear) | 1.892x | +24.6% |

SmartDCA (Quadratic) | 2.105x | +38.7% |

SmartDCA (Bounded/tanh) | 2.328x | +53.4% |

Table: SmartDCA variants vs Standard DCA — Bitcoin Backtest. Source: Calvet et al. (2023), arXiv:2308.05200

Figure 3: SmartDCA variants consistently outperform standard DCA on Bitcoin (2017–2023). Source: Calvet, Herranz-Celotti & Valimamode (2023).

Marshall (2000): Statistical Comparison Across Traditional Markets

Paul Marshall's 2000 paper in the Journal of Financial and Strategic Decisions provided one of the earliest rigorous comparisons using Monte Carlo simulation and multiple performance metrics. His key finding: value averaging provides superior expected investment returns when prices are volatile and over extended time horizons, with little or no increase in risk.

Critically, Marshall noted that prior VA studies relied on Internal Rate of Return (IRR), which can be misleading for strategies with variable cash flows. Using continuously compounded returns, the advantage of VA over DCA narrowed but remained positive, particularly in high-volatility environments — precisely the conditions crypto markets exhibit.

Value Averaging vs DCA: A Structured Comparison

Parameter | Fixed Amount DCA | Value Averaging |

Investment per period | Fixed (e.g., ₹1,000/month) | Variable (adjusts to meet target value) |

Decision rule | Invest same amount regardless of price | Invest more when price falls, less when it rises |

Cash flow predictability | Fully predictable | Unpredictable — requires cash buffer |

Average cost basis | Harmonic mean of prices | Below harmonic mean (mathematically proven) |

Performance in volatile markets | Good — benefits from buying dips passively | Better — actively capitalises on dips |

Performance in bull markets | Good — maintains full exposure | Weaker — reduces buying when prices rise |

Complexity | Minimal — set and forget | Moderate — requires monthly calculations |

Bitcoin backtest (2010–2019) | Baseline returns | +20% higher returns (beat DCA every year) |

Automation availability (India) | All major exchanges (CoinDCX, CoinSwitch, Mudrex) | Not available on any platform currently |

Table: Value Averaging vs Fixed Amount DCA — Full Comparison

The Limitations of Value Averaging in Crypto

The research is clear on returns. But returns are not the only variable that matters. Value averaging has practical limitations that become amplified in crypto's extreme volatility environment.

1. Cash Reserve Requirement

Value averaging requires maintaining a side cash reserve from which to make variable investments. In a steep crypto drawdown (30–50% in weeks, not uncommon), the strategy demands significantly more capital than planned. An investor budgeting ₹10,000/month might need to deploy ₹25,000–30,000 in a single month during a crash. If the cash reserve is exhausted, the strategy breaks.

2. Unpredictable Cash Flows

Salaried investors in India typically have fixed monthly surpluses. DCA aligns perfectly with this reality. Value averaging does not. You cannot know in advance how much you will need to invest each month. This creates a mismatch between salary cycles and investment requirements.

3. Underperformance in Strong Bull Markets

When prices rise sharply and consistently (as Bitcoin did in 2017 and 2021), value averaging reduces purchases or stops buying entirely. The investor ends up with less exposure during the rally. In crypto's asymmetric return distribution — where the majority of gains come from a few explosive months — this is a meaningful cost.

4. IRR Bias (Academic Criticism)

Simon Hayley at Bayes Business School (formerly Cass) has shown that the IRR metric — used in many older VA studies — contains a systematic hindsight bias for strategies that link investment size to past performance. This inflates VA's apparent advantage. When measured using time-weighted return or continuously compounded return, the gap narrows.

5. No Platform Support in India

As of May 2026, no Indian crypto exchange offers automated value averaging. Every "crypto SIP" product is fixed-amount DCA. Implementing VA requires manual monthly calculations and execution — friction that most retail investors will not sustain over multi-year horizons.

The Indian Crypto SIP Landscape: Where Value Averaging Fits

India's crypto SIP market exploded in 2025. The numbers tell the story:

Platform | SIP Growth (2025) | Avg Investment |

CoinDCX | 572,000+ new SIPs (~600% YoY) | ₹100/month |

CoinSwitch | +59% growth in new SIPs | Not disclosed |

Mudrex | +220% surge in SIP openings | ₹4,000–₹6,000/month |

Table: India's Crypto SIP Growth in 2025. Source: Moneycontrol, TradingView, CCN.

All of these are fixed-amount DCA. Every single one. The opportunity for a platform to offer intelligent, value-averaging-based systematic investing remains entirely unaddressed.

For investors who want the benefits of smart systematic strategies without manual execution, professionally managed crypto portfolios — such as those offered by platforms like Grade Capital — can incorporate dynamic allocation principles at the fund level. Rather than requiring investors to calculate and adjust monthly instalments manually, a managed approach applies these optimisation strategies within the portfolio management process itself.

Tax Implications: DCA and Value Averaging Under Indian Law

Both DCA and value averaging create multiple purchase lots over time. Under India's current VDA tax framework, each lot is treated independently:

· Section 115BBH: Flat 30% tax on gains from each VDA transaction. No loss offset. No carry-forward. FIFO (First In, First Out) method applies.

· Each SIP instalment = separate tax lot: Whether you invest ₹1,000 (DCA) or ₹2,500 (VA) in a given month, each purchase creates its own cost basis.

· Value averaging's higher variability = more complex record-keeping: Tracking cost basis across irregular investment amounts requires more diligent documentation.

An alternative structure: crypto derivatives (futures and options) are taxed as speculative business income under Section 43(5) and Section 73 — not as VDA capital gains. This means slab-rate taxation, expense deductions, and 4-year loss carry-forward. Platforms like Grade Capital use this derivatives-based structure for their managed crypto portfolios.

Tax treatment depends on individual circumstances and the prevailing interpretation of tax laws. Investors are advised to consult with qualified tax professionals to understand how these provisions apply to their specific situation.

Which Strategy Should You Choose?

The answer depends on three variables: your cash flow predictability, your risk tolerance for variable commitments, and your time horizon.

Choose fixed-amount DCA if: you have a fixed monthly surplus, want zero complexity, and are comfortable with slightly lower returns in exchange for absolute predictability. This is most salaried investors in India.

Choose value averaging if: you have irregular or surplus income, can maintain a 2–3x cash buffer beyond your monthly target, are willing to do monthly calculations, and have a time horizon of 3+ years. Entrepreneurs, freelancers, and HNIs with variable cash flows are natural candidates.

Choose a managed approach if: you want the benefits of intelligent allocation strategies without manual execution. Professionally managed crypto portfolios incorporate dynamic rebalancing, derivatives-based hedging, and risk-adjusted allocation — effectively applying smart systematic principles at an institutional level.

The Bottom Line

Value averaging is not a new idea. It is a 38-year-old strategy with rigorous academic support, mathematically proven to achieve a lower average cost than fixed-amount DCA. In crypto — where volatility is structural, not occasional — its advantage is amplified.

The gap between what research recommends and what Indian crypto platforms offer represents both a risk and an opportunity. Until automated VA products exist, investors can implement value averaging manually or seek managed portfolio solutions that incorporate these principles professionally.

The question is not whether value averaging works in crypto. The data is settled. The question is whether you have the discipline, cash reserves, and infrastructure to execute it consistently.

Past performance is not indicative of future results. The returns presented are historical and may not be repeated. This content is for informational and educational purposes only and does not constitute financial advice or an offer to invest.