Every crypto exchange in India now offers a "Crypto SIP" feature. CoinDCX created over 572,000 new SIPs in 2025. CoinSwitch saw a 59% jump. Mudrex recorded 220% growth. The pitch is familiar — invest a fixed amount every week or month, ride out volatility, build wealth over time.

That pitch is not new. It is dollar cost averaging — a strategy Benjamin Graham described in The Intelligent Investor in 1949. DCA and crypto SIP are mechanically identical. But the structures around them — regulation, tax treatment, investor protection, and risk management — are not even close.

This distinction matters. Especially in India, where the term "SIP" carries institutional weight borrowed from a SEBI-regulated mutual fund ecosystem. Calling a recurring crypto purchase a "SIP" implies protections that do not exist.

What Is Dollar Cost Averaging (DCA)?

Dollar cost averaging is a disciplined investment strategy where an investor commits a fixed amount of money to a single asset at regular intervals — weekly, fortnightly, or monthly — regardless of the asset’s current price. When the price drops, the fixed amount buys more units. When it rises, fewer units are purchased.

The mathematical result is that the investor’s average cost per unit converges to the harmonic mean of the prices over time — always lower than or equal to the arithmetic mean. Calvet et al. (2023) proved this formally using the Cauchy–Schwarz inequality in their paper "SmartDCA Superiority" published on arXiv.

DCA is not an Indian invention. It is not a crypto invention. It is a decades-old principle applied across equities, bonds, ETFs, commodities, and now digital assets.

What Is a Crypto SIP in India?

A crypto SIP is an automated recurring purchase of cryptocurrency on an Indian exchange. Platforms like CoinDCX (CIP — Crypto Investment Plan), CoinSwitch, and Mudrex allow users to set a fixed rupee amount starting from as low as ₹50–₹100, pick a frequency (daily, weekly, monthly), and let the system execute purchases automatically.

The underlying mechanism is DCA. The branding is SIP — borrowed directly from India’s mutual fund industry, where SIP has become synonymous with disciplined long-term investing.

Feature | Mutual Fund SIP | Crypto SIP |

Regulator | SEBI | FIU-IND (PMLA only) |

Asset custody | Custodian/Trust | Exchange wallet |

NAV pricing | Standardised daily NAV | Market price at execution |

Investor protection | SEBI grievance redressal | None |

Tax treatment | LTCG/STCG with indexation | Flat 30% (Sec 115BBH) |

Loss offset | Yes (within asset class) | No — zero offset |

Minimum amount | ₹100–₹500 | ₹50–₹100 |

Lock-in | ELSS: 3 years; others: none | None |

Insurance/guarantee | AMFI / DICGC framework | None |

Table 1: Structural Comparison — Mutual Fund SIP vs Crypto SIP in India

The table above is the critical difference. A mutual fund SIP operates within a SEBI-regulated trust structure where your money is held by a custodian, separate from the AMC’s balance sheet. A crypto SIP sits on an exchange’s wallet infrastructure with no equivalent separation.

What the Research Says About DCA in Crypto

Three rigorous studies provide the evidentiary backbone for understanding DCA’s effectiveness in volatile assets like cryptocurrency.

Vanguard (2023): Lump Sum Beats DCA 68% of the Time

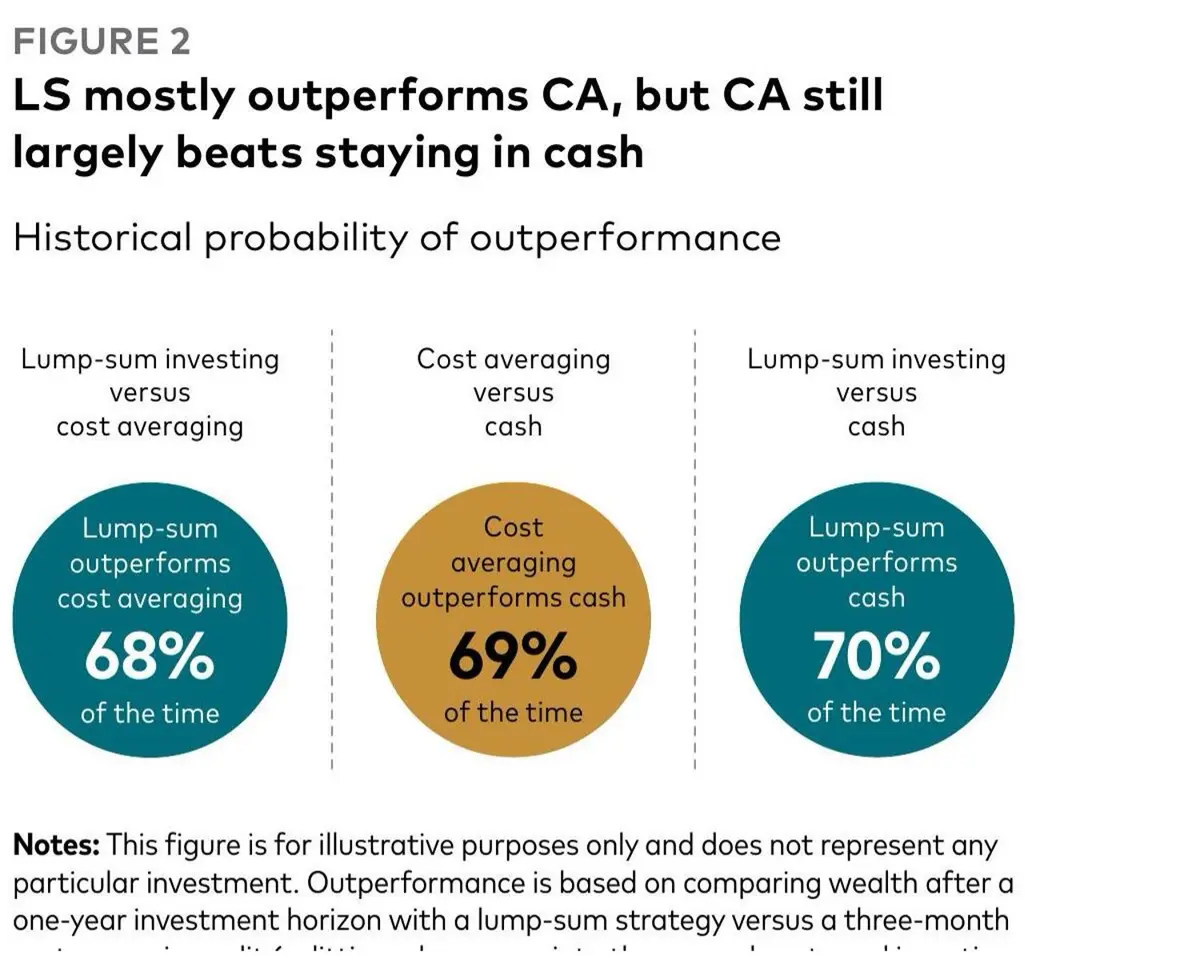

Vanguard’s landmark 2023 study analysed historical and simulated returns across the US, UK, Canada, Europe, and Australia from 1976 to 2022. The headline finding: lump sum investing outperformed cost averaging (DCA) roughly two-thirds of the time. Across global markets using MSCI World Index returns, lump sum beat DCA 67.7% of the time for a 3-month split, rising to 72.6% for a 6-month split.

Figure 1: Vanguard Research — Lump sum outperforms DCA 68% of the time, but DCA still beats cash 69% of the time. Source: Vanguard (2023)

But the study also found that DCA still beats holding cash 69% of the time. For investors with significant loss aversion, DCA reduces regret and drawdown exposure. At the median, a lump sum 100% equity portfolio yielded 2.2% more wealth after one year — meaningful, but not transformative.

The takeaway for crypto investors: if you have a lump sum and high conviction, deploying it immediately has historically produced better results. If you receive income monthly and want market exposure without timing risk, DCA is the rational second-best.

NUS Singapore (2022): 3-Year Bitcoin DCA — 100% Profitable

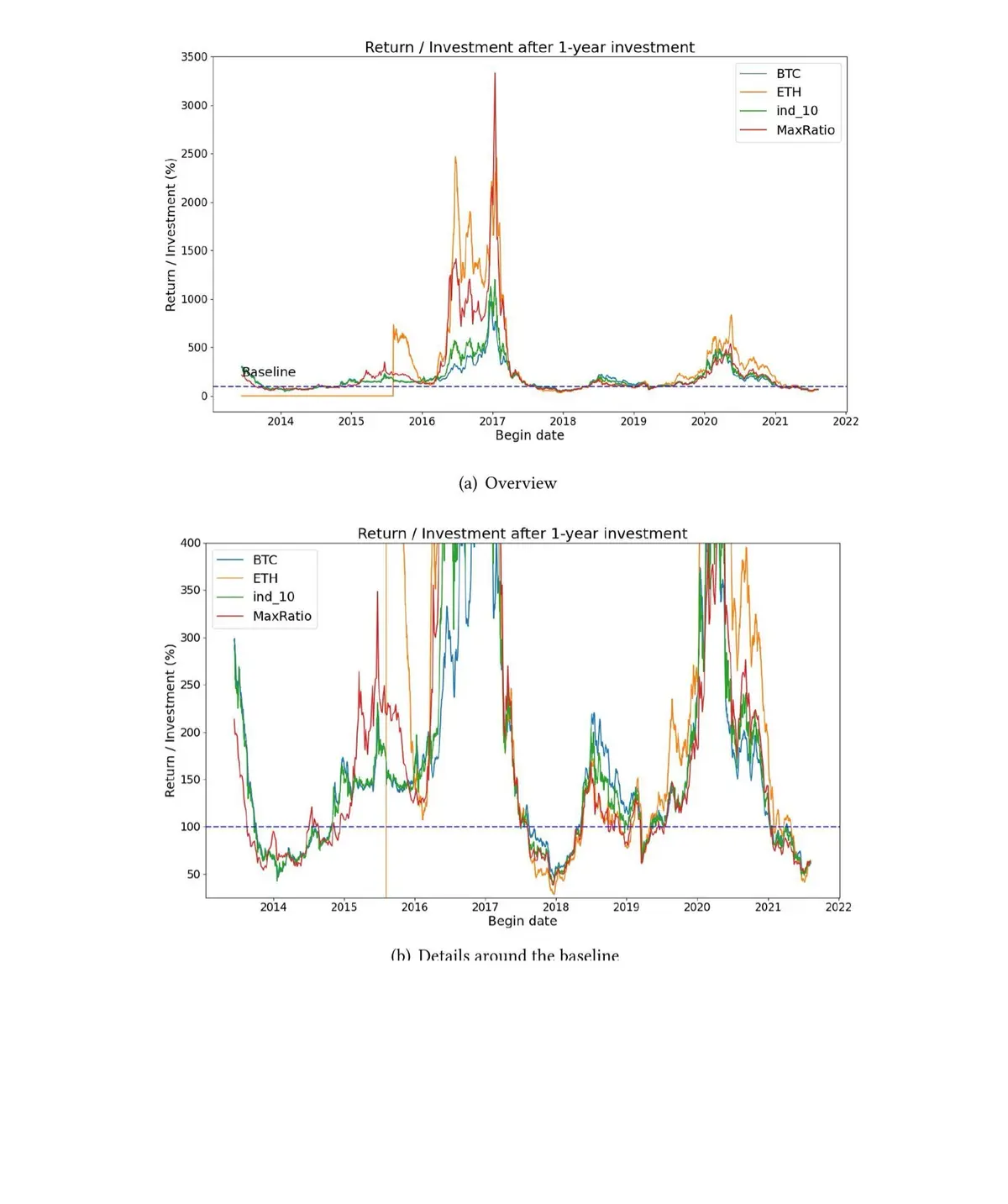

Shanmu Wang’s 2022 study at the National University of Singapore backtested DCA strategies on Bitcoin, Ethereum, and a top-10 crypto index using CoinMarketCap price data from 2013 to 2022. The simulation invested $100 every 10 days and measured Return/Investment ratios across 1-year, 2-year, and 3-year holding periods.

Holding Period | BTC Profitable | BTC >150% Return | BTC >300% Return | ETH >300% Return |

1 Year | 76.4% | 41.3% | 11.1% | 24.4% |

2 Years | 93.4% | 88.6% | 44.7% | 70.8% |

3 Years | 100% | 88.5% | 69.9% | 91.8% |

Table 2: Bitcoin and Ethereum DCA Return Probabilities by Holding Period. Source: Wang (2022), NUS CP3106

Figure 2: DCA backtesting results for BTC, ETH, and crypto index portfolios — 1-year investment horizon. Source: Wang (2022), NUS

The data is stark. Every rolling 3-year DCA window for Bitcoin ended in profit. The probability of exceeding a 300% return over three years was 69.9% for BTC and 91.8% for ETH. Even investors who started at the December 2017 peak — the worst possible entry — recovered fully within the 3-year window.

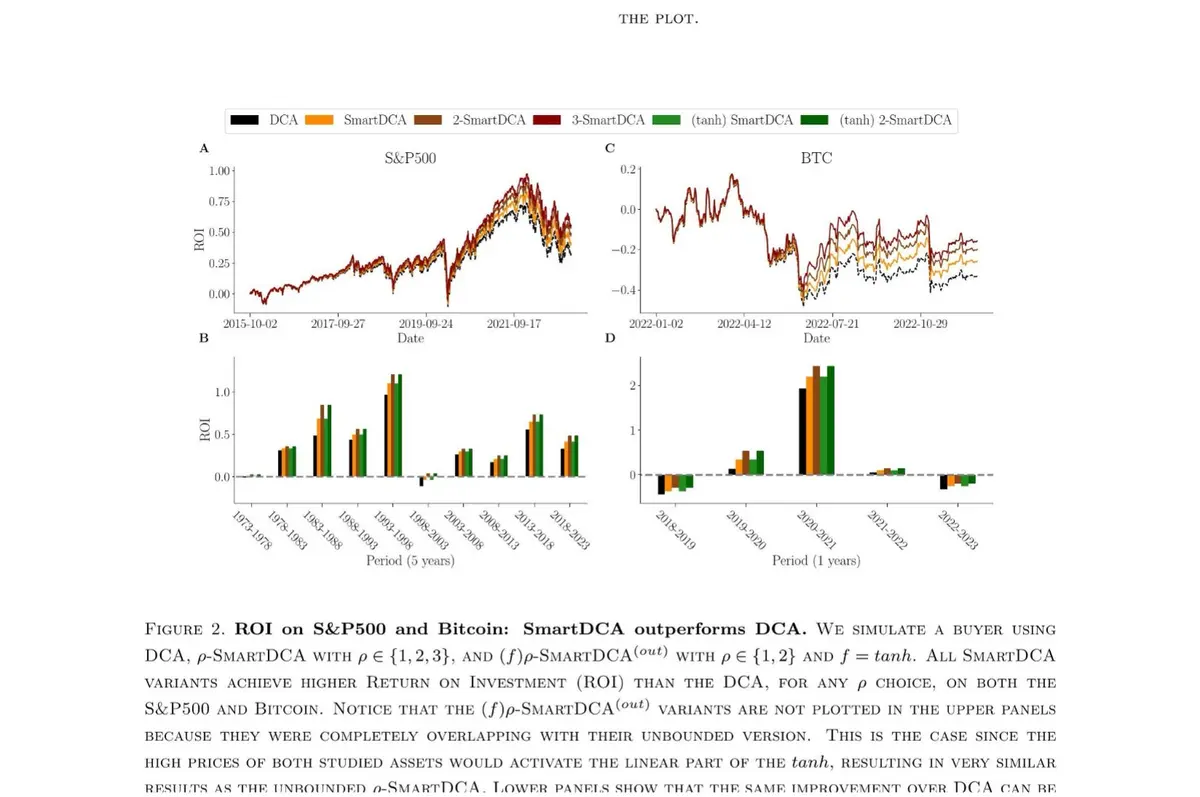

SmartDCA (2023): A Mathematically Proven Improvement

Calvet, Herranz-Celotti, and Valimamode (2023) did not just test DCA — they improved it. Standard DCA invests a fixed dollar amount regardless of price, yielding the harmonic mean cost per unit. SmartDCA invests an amount inversely proportional to the current price — allocating more capital when prices are low and less when they are high.

The result, proven via the Cauchy–Schwarz inequality, is that SmartDCA always achieves a lower average cost per unit than standard DCA. This holds for any number of buying events, any asset, any market condition.

Strategy | Avg Cost per BTC | Total Invested | ROI |

Standard DCA | $10,942.80 | $1,827 | 1.518 |

(sig+) SmartDCA | $8,893.60 | $516.30 | 1.868 |

(tanh) SmartDCA | $7,134.80 | $0.166 | 2.328 |

3-SmartDCA | $4,790.50 | $4,180.90 | 3.460 |

Table 3: DCA vs SmartDCA Variants — Bitcoin Backtest (2017–2023). Source: Calvet et al. (2023)

Figure 3: SmartDCA consistently outperforms standard DCA on both S&P 500 and Bitcoin across all time periods. Source: Calvet et al. (2023)

The bounded (tanh) SmartDCA variant achieved an ROI of 2.328 versus standard DCA’s 1.518 — a 53% improvement — while keeping total investment within reasonable bounds. For investors already committed to DCA, these findings suggest that price-weighted allocation is a quantifiably better approach.

India’s Crypto SIP Boom: The Numbers

India’s crypto SIP adoption accelerated sharply in 2025. Exchange-level data tells the story.

Platform | SIP Growth (2025) | New SIPs Created | Avg Ticket Size |

CoinDCX | +600% YoY | 572,000+ | ₹100/month |

CoinSwitch | +59% YoY | Not disclosed | BTC, ETH, SOL, XRP focused |

Mudrex | +220% YoY | Not disclosed | ₹4,000–₹6,000/month |

Table 4: Crypto SIP Growth Across Indian Exchanges in 2025. Sources: TradingView/Moneycontrol, Yahoo Finance

The aggregate growth exceeded 60% year-on-year. Bitcoin remained the most popular SIP asset on CoinDCX, followed by Ethereum and Solana. Entry points have dropped to as low as ₹50 per cycle, mirroring the accessibility of mutual fund SIPs.

A separate data point reinforces the trend: a $10 weekly Bitcoin DCA from 2019 to 2024 — a total investment of $2,620 — returned $7,913, a 202% gain. That outperformed the S&P 500 by roughly 3x over the same period, according to Nasdaq data.

The Regulatory Gap: Why Calling It a "SIP" Is Misleading

The word "SIP" in India does not just describe a method. It describes a regulated framework. When an investor sets up a SIP through HDFC AMC or Axis Mutual Fund, they are entering a SEBI-regulated ecosystem with specific investor protections.

Protection Layer | Mutual Fund SIP | Crypto SIP |

Primary regulator | SEBI | None (FIU-IND for AML only) |

Asset custody | Held in trust by custodian | Held on exchange wallet |

AMC/Exchange failure | SEBI appoints new manager | No mandated recovery process |

NAV computation | Daily, standardised, audited | Market price at order execution |

Grievance redressal | SEBI SCORES portal | None |

Scheme disclosure | Mandatory SID, KIM, factsheet | No equivalent requirement |

Exit load transparency | SEBI-mandated disclosure | Platform-specific; varies |

Insurance | DICGC framework (debt funds) | None |

Table 5: Investor Protection Comparison — Mutual Fund SIP vs Crypto SIP

SEBI’s updated Mutual Fund Regulations 2026 further strengthened protections — lower expense ratios, revised brokerage limits, and enhanced disclosure requirements. Crypto exchanges, by contrast, are required only to register with FIU-IND under the Prevention of Money Laundering Act. This covers KYC and suspicious transaction reporting. It does not cover investment protection, NAV standardisation, or custodial separation.

The regulatory conversation is evolving. Reports suggest SEBI is expected to act as the primary supervisor for crypto exchanges, with the RBI overseeing cross-border capital flows. But as of May 2026, no formal crypto investment regulation exists.

Tax Implications: Each Crypto SIP Instalment Is a Separate Tax Event

This is where the mechanical similarity between DCA and crypto SIP becomes a tax accounting challenge. Under Section 115BBH, every crypto purchase creates a separate tax lot. When you sell, the gain or loss on each lot is calculated independently using FIFO (First In, First Out) methodology.

Tax Parameter | Mutual Fund SIP | Crypto SIP |

Tax rate | LTCG 12.5% / STCG 20% | Flat 30% + 4% cess |

Loss offset | Yes (within equity/debt class) | No — zero offset allowed |

Loss carry-forward | Up to 8 years (equity LTCG) | No carry-forward |

TDS on transfer | None | 1% TDS (Section 194S) |

Cost of acquisition | NAV-based, clear | Market price at execution time |

Expense deduction | Limited (management fees built in) | None |

ITR form | ITR-2 (Capital Gains) | ITR-2 (VDA schedule) |

Table 6: Tax Treatment — Mutual Fund SIP vs Crypto SIP in India

Consider a simple example: an investor runs a monthly crypto SIP of ₹5,000 for 12 months. That creates 12 separate tax lots. If six lots are profitable and six are loss-making, the losses cannot offset the gains. Tax is owed on the full profit from the six winning lots. The six losing lots produce no tax benefit whatsoever.

This is a structural disadvantage that has no parallel in the mutual fund SIP ecosystem.

How Grade Capital Approaches This

Grade Capital’s managed crypto derivatives fund offers a fundamentally different structure. Rather than executing direct spot purchases through a SIP, the fund deploys capital into crypto derivatives — futures and options — with professionally managed hedging strategies.

Three structural advantages distinguish this approach from a standard crypto SIP.

Tax efficiency. Crypto derivatives income is classified as speculative business income under Section 43(5), taxed at the investor’s income tax slab rate — not the flat 30% VDA tax. Losses can offset gains, and unused losses carry forward for up to four years.

Professional risk management. DCA mitigates entry timing risk. It does nothing for downside risk once invested. Grade Capital’s fund uses options positions and dynamic hedging to generate returns even in falling markets — a capability that no SIP structure can replicate.

Institutional-grade custody. Assets are held through Fireblocks (SOC 2 Type II, ISO 27001) with MPC wallet technology, 80% cold storage, and insurance from A-rated carriers. This is custodial separation — the kind of structural protection that crypto SIPs on exchanges do not provide.

Past performance is not indicative of future results. The returns presented are historical and may not be repeated.

DCA vs Lump Sum vs Value Averaging: A Strategy Matrix

DCA is not the only systematic approach. Investors should understand how it compares to lump sum investing and value averaging — the third option that rarely gets discussed.

Strategy | How It Works | Best For | Evidence |

DCA | Fixed amount at fixed intervals | Salaried investors, risk-averse | Harmonic mean cost; NUS: 100% profitable over 3 yrs |

Lump Sum | Deploy full capital immediately | High-conviction, long time horizon | Vanguard: outperforms DCA 68% of the time |

Value Averaging | Adjust amount to hit target portfolio value | Experienced investors | Higher returns in volatile markets; complex execution |

SmartDCA | Invest inversely proportional to price | Quant-oriented investors | Calvet (2023): 53% higher ROI than standard DCA on BTC |

Table 7: Investment Strategy Comparison Matrix

The Vanguard wealth comparison above shows that lump sum investing produces higher 95th percentile outcomes but also lower 5th percentile outcomes. DCA narrows the distribution — lower ceiling, higher floor. For investors who prioritise not losing sleep over maximising terminal wealth, DCA remains the pragmatic choice.

Should You Use a Crypto SIP? A Decision Framework

Before setting up a crypto SIP on any Indian exchange, consider five factors.

Regulatory risk. Your assets sit on an exchange wallet with no SEBI-mandated custodial separation. If the exchange faces operational issues, your recourse is limited.

Tax complexity. Each instalment is a separate tax lot. With 12 monthly SIPs, you have 12 cost bases to track. FIFO applies, and losses cannot offset gains.

Volatility exposure. DCA smooths entry price, but crypto can drop 70–80% in a bear cycle. DCA does not protect against sustained drawdowns.

Platform fees. While some exchanges offer zero-fee SIPs, the effective cost includes spread, withdrawal fees, and TDS leakage at 1%.

Alternative structures. Managed portfolio solutions like Grade Capital offer exposure to crypto returns with professional risk management, tax efficiency, and institutional custody — structural advantages a SIP cannot provide.

The Bottom Line

DCA and crypto SIP describe the same action — investing a fixed amount at regular intervals. The strategy is sound. The evidence supports it. Over three years, a Bitcoin DCA has never lost money in any rolling window since 2013.

But the packaging matters. In India, "SIP" implies a regulated, protected, standardised framework. Crypto SIPs operate outside that framework. The 30% flat tax with no loss offset, the absence of SEBI oversight, and the lack of custodial separation are not minor details. They are structural gaps.

For investors who want crypto exposure with professional management, tax efficiency, and institutional-grade custody, Grade Capital’s managed crypto derivatives fund offers a structure that addresses these gaps directly.

Explore how Grade Capital’s managed portfolios work at www.grade.capital

This content is for informational and educational purposes only and does not constitute financial advice or an offer to invest.