Last Updated: June 2026

Crypto for Salaried Employees in India: A Realistic Rs 5,000/Month Plan After Tax

Crypto for salaried employees India is no longer a question of whether it makes sense — the research now says it does, even at very small allocations. Fidelity Digital Assets' 2026 research paper "Getting Off Zero" found that the most significant improvement in a portfolio's Sharpe ratio occurs at just 1-3% Bitcoin allocation. For a salaried employee earning Rs 10 LPA with Rs 77,500/month in-hand, a Rs 5,000 monthly crypto allocation represents 6.5% of take-home pay — well within what the RBI reports as India's household financial savings rate of 5.1% of Gross National Disposable Income.

This article builds a realistic, after-tax crypto investment plan for salaried Indians — grounded in institutional research, DCA backtests, and actual Indian tax law — not social media advice or influencer opinions.

The Salaried Investor's Starting Point: How Much Can You Actually Spare?

Before allocating anything to crypto, a salaried investor needs to understand what Rs 5,000/month actually means relative to their income. The numbers are more favourable than most people assume.

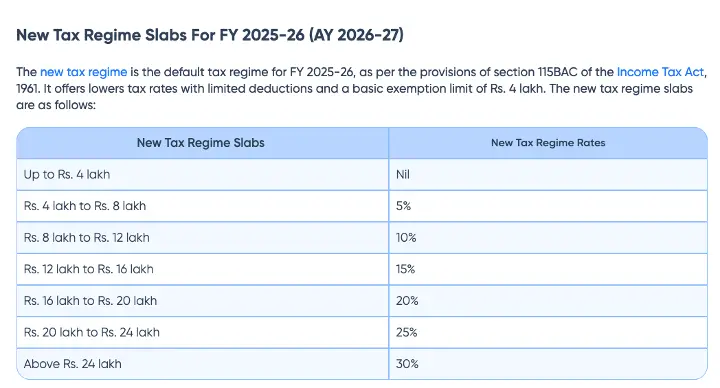

The average urban professional salary in India is Rs 7-9 LPA. At Rs 10 LPA CTC, the in-hand salary under the new tax regime is approximately Rs 77,500/month — roughly 65-75% of CTC after EPF, professional tax, and income tax deductions. The new tax regime for FY 2025-26 (Section 115BAC) offers zero tax on income up to Rs 12 lakh, with a standard deduction of Rs 75,000 — making Rs 12.75 lakh effectively tax-free.

Source: ClearTax — New Tax Regime Slabs for FY 2025-26 (AY 2026-27). Income up to Rs 4 lakh is nil, Rs 4-8 lakh at 5%, Rs 8-12 lakh at 10%, with progressively higher rates above Rs 12 lakh.

Component | Rs 10 LPA CTC | Rs 7 LPA CTC |

Monthly CTC | Rs 83,333 | Rs 58,333 |

EPF (12% of Basic) | Rs 5,000-6,000 | Rs 3,500-4,200 |

Professional Tax | Rs 200 | Rs 200 |

Income Tax (New Regime) | Rs 0-1,000 | Rs 0 |

Approx. In-Hand | Rs 77,500 | Rs 54,000 |

Essential Expenses (60%) | Rs 46,500 | Rs 32,400 |

Savings & Investments (25%) | Rs 19,375 | Rs 13,500 |

Crypto Allocation (Rs 5,000) | 6.5% of in-hand | 9.3% of in-hand |

At Rs 10 LPA, Rs 5,000/month is 6.5% of in-hand income — comfortably within the savings bucket. At Rs 7 LPA, it stretches to 9.3%, which is still feasible but requires tighter budgeting. The RBI's 2023-24 data shows Indian households save 5.1% of GNDI in net financial assets (gross savings are 11.2%), with total household financial savings at Rs 54.6 lakh crore. The Rs 5,000/month plan fits within these established savings patterns — it is not an extreme allocation.

Prerequisite: This plan assumes a 3-6 month emergency fund is already in place. Crypto is a satellite allocation (5-10% of investable surplus), not a replacement for fixed deposits, EPF, or health insurance. If your EMIs exceed 40% of in-hand income, build that buffer first.

What Institutional Research Says About Small Crypto Allocations

The most compelling argument for a salaried employee to allocate even Rs 5,000/month to crypto does not come from crypto Twitter or YouTube. It comes from institutional research papers that most retail investors have never read.

Fidelity Digital Assets: "Getting Off Zero" (2026)

Source: Fidelity Digital Assets — "Getting Off Zero: Evaluating Bitcoin in 2026" by Chris Kuiper, CFA. A research study examining Bitcoin's role in modern investment portfolios.

Fidelity Digital Assets' research paper, authored by Chris Kuiper CFA, makes several findings that are directly relevant to salaried investors considering a small monthly allocation:

Bitcoin was the top-performing asset in 11 of the last 15 years. Not in all years — the 4 underperforming years included some of the worst drawdowns in any asset class. But across a 15-year window, no other asset appeared at the top as frequently.

The most significant Sharpe ratio improvement occurs at 1-3% allocation. Adding just 1-3% Bitcoin to a traditional 60/40 equity-bond portfolio improved risk-adjusted returns more meaningfully than any larger allocation increment. This is the "sweet spot" — enough to matter, not enough to destabilise.

87% r-squared between global M2 money supply and Bitcoin price. This correlation suggests Bitcoin's long-term price is driven by global monetary expansion — not by speculation alone. As central banks continue to expand money supply, Bitcoin's structural case strengthens.

Kelly Criterion analysis suggests up to 10% allocation under conservative assumptions (25% expected return, 50% volatility). The Kelly Criterion is a mathematical formula used by institutional investors to determine optimal position sizing. Even under deliberately cautious inputs, it recommends a non-trivial allocation.

CFA Institute and Vanguard: The Academic Consensus

The CFA Institute Research Foundation published a guide for investment professionals noting that crypto assets have low correlations with traditional asset classes, supporting the diversification case even at small allocations. Meanwhile, Vanguard's 2012 landmark whitepaper on dollar-cost averaging found that lump sum investing beats DCA 67% of the time across US, UK, and Australian markets — with a 2.3% average advantage over 12-month periods. However, Vanguard's own conclusion acknowledged that for volatile assets where behavioral discipline matters, DCA provides guardrails that prevent the common mistake of buying at the top and panic-selling at the bottom.

For a salaried employee investing Rs 5,000/month from a fixed salary, DCA is not a choice — it is the default. The salary arrives monthly, and the investment follows. The question is not whether to DCA, but how to do it most effectively.

DCA Backtests: What Rs 5,000/Month Would Have Actually Returned

Theory is useful. Data is better. Here is what systematic Bitcoin DCA has actually returned over different time periods, based on verified backtest data from dcabtc.com and SpotedCrypto's 12-year analysis.

DCA Period | Amount Invested | Portfolio Value | Return | Source |

10 years ($100/month since 2014) | $35,700 (approx. Rs 30 lakh) | $589,000 (approx. Rs 5 crore) | 1,648% | |

5 years ($10/week, 2019-2024) | $2,610 (approx. Rs 2.2 lakh) | $7,913 (approx. Rs 6.7 lakh) | 202% | |

7 years (fear-based DCA) | Variable (buy at Fear & Greed < 25) | Outperformed standard | 1,145% vs 1,046% buy-and-hold | SpotedCrypto |

12 years (fear-based DCA) | Variable | Significantly outperformed | 6,712% | SpotedCrypto |

The NUS Singapore academic paper by Shanmu Wang took DCA further. Using reinforcement learning (Rainbow DQN), the research found that machine-optimised DCA improved profits by 2-4% over standard fixed-interval DCA. More practically, the paper quantified something many investors sense intuitively: there is approximately a 40% probability of achieving a 150% gain with 1-year Bitcoin DCA, rising to approximately 80% when the DCA period extends to 2 years.

What does this mean for a Rs 5,000/month plan? At today's exchange rates, Rs 5,000 is approximately $60. Based on the 5-year DCA backtest (202% return), Rs 5,000/month for 5 years (Rs 3 lakh total invested) could potentially grow to approximately Rs 9 lakh — before taxes. The 10-year numbers are more dramatic, but the 5-year window is more relevant for most salaried investors' planning horizons.

Fear-based DCA — buying only when the market is in extreme fear — has historically outperformed standard DCA. The SpotedCrypto analysis showed buying only when the Fear & Greed Index drops below 25 returned 1,145% over 7 years vs 1,046% for buy-and-hold — and an extraordinary 6,712% over a 12-year backtest window. For salaried investors, a modified approach works well: invest Rs 5,000/month as the base, and add a Rs 5,000-10,000 "fear bonus" from savings when the index drops below 25.

The Rs 5,000/Month Plan: A Step-by-Step Structure

A plan without structure is just a wish. Here is a concrete framework for salaried employees to implement a Rs 5,000/month crypto allocation.

Step 1: Segregate on Salary Day

Set up an auto-transfer of Rs 5,000 from your salary account to a dedicated savings account (or directly to your investment platform) on salary credit day. Behavioural finance research consistently shows that automation removes decision fatigue — the single biggest enemy of consistent investing. Treat it like an EMI: non-negotiable, pre-committed, invisible.

Step 2: Choose Your Method

Option A: Direct DCA on an exchange. Buy Bitcoin (or a mix of BTC + ETH) on the 1st or 15th of every month on a platform like CoinDCX or Mudrex. Simple, but taxed at 30% flat on gains under Section 115BBH.

Option B: Managed crypto derivatives portfolio. Platforms like Grade Capital offer managed derivatives exposure where gains are taxed as speculative business income at slab rates under Section 43(5) — potentially saving 40-60% in taxes compared to spot crypto. The minimum investment starts at Rs 12,000 lumpsum.

Option C: Split allocation. Rs 2,500 in direct BTC DCA (for conviction) + Rs 2,500 in a managed fund (for diversification and tax efficiency). This balances direct ownership with professional risk management.

Step 3: Review Quarterly, Not Daily

The entire purpose of a Rs 5,000/month DCA plan is to remove the need for daily monitoring. Check your portfolio once a quarter. Review your allocation once a year. The salaried investor's edge is patience and consistency — not market timing. India has 119 million crypto owners, yet 72% are under 35. Time is the most valuable asset young salaried investors possess, and DCA converts it into compound returns.

Tax Framework: What Every Salaried Crypto Investor Must Know

This is where most salaried crypto investors make their most expensive mistake: ignoring the tax implications until filing season. Understanding the framework before investing saves real money.

The Three Tax Regimes for Crypto in India

1. Spot Crypto (Section 115BBH): Flat 30% tax on all VDA gains — no deductions, no loss offset, no carry-forward. Plus 4% health and education cess. Plus 1% TDS on every transaction under Section 194S (claimable as refund while filing ITR, but still a cash flow drag).

2. Crypto Derivatives (Section 43(5)): Taxed as speculative business income at your income slab rate. Business expenses deductible. Losses offset against other speculative income. Four-year loss carry-forward. No TDS. Filed under ITR-3.

3. Bitcoin ETF via LRS (Foreign Asset): 12.5% LTCG after 24 months holding period (classified as foreign asset, not VDA). But requires LRS remittance ($250,000/year limit), 20% TCS on amounts above Rs 7 lakh, and USD conversion costs.

Tax Math on Your Rs 5,000/Month Plan

Assume Rs 5,000/month for 12 months = Rs 60,000 invested. Assume a 100% return (conservative for a good year) = Rs 60,000 gain. Here is what you actually pay:

Tax Parameter | Spot Crypto (Sec 115BBH) | Derivatives (Sec 43(5)) | BTC ETF via LRS |

Tax Rate | 30% flat + 4% cess | Slab rate (0-30%) | 12.5% LTCG (after 24 months) |

Tax on Rs 60,000 Gain | Rs 18,720 (31.2%) | Rs 0-3,000 (0-5% slab) | Rs 7,500 (12.5%) |

Expense Deduction | Not allowed | Allowed | Not applicable |

Loss Offset | Not allowed | Against speculative income | Against LTCG from other assets |

TDS | 1% on every transfer | None | None (US broker) |

Currency Conversion Cost | None | None | 1-2% (INR to USD and back) |

Minimum Access | Rs 100 | Rs 12,000 (Grade Capital) | $250+ (LRS brokerage) |

Net Take-Home (on Rs 60,000 gain) | Rs 41,280 | Rs 57,000-60,000 | Rs 51,000-52,500 |

The difference is stark. On a Rs 60,000 gain, spot crypto leaves you with Rs 41,280 after tax. Crypto derivatives through a managed portfolio could leave you with Rs 57,000-60,000 — a Rs 15,000-18,000 annual saving just from tax structure, on the same underlying asset class. Over 5 years, that compounds significantly.

The new tax regime makes this even more attractive for salaried employees. With income up to Rs 12.75 lakh effectively tax-free, a salaried employee earning Rs 10 LPA whose derivatives gains fall within the lower slabs could pay as little as 0-5% tax on crypto profits — versus the non-negotiable 30% flat rate on spot.

Risk Guardrails for Salaried Investors

No discussion of crypto investing is complete without risk — and salaried employees have less margin for error than HNIs or entrepreneurs. Here are the non-negotiable guardrails:

Never invest more than you can afford to lose entirely. Bitcoin's maximum historical drawdown is approximately 77.6% (2021-2022). Rs 5,000/month invested during a peak could decline to Rs 1,120/month in portfolio value before recovering. If that thought causes panic, reduce the allocation.

Crypto has no deposit insurance. Unlike bank deposits protected by DICGC up to Rs 5 lakh, crypto holdings on exchanges carry counterparty risk. The WazirX hack is a recent reminder. Consider platforms with institutional-grade custody (such as Fireblocks, which holds SOC 2 Type II and ISO 27001 certifications) or self-custody for long-term holdings.

Satellite, not core. Financial planners recommend crypto as a 5-10% satellite allocation within investable surplus. For a salaried employee with Rs 19,375/month in savings (25% of Rs 77,500 in-hand), Rs 5,000 is 25.8% of the savings bucket — which is the upper limit. Do not go higher unless your emergency fund, health insurance, and EPF contributions are fully funded.

File your ITR even if below the taxable threshold. Section 194S mandates 1% TDS on VDA transfers. This TDS shows up in your Form 26AS. Even if your total income is below the taxable limit, you must file ITR to claim the TDS refund. Missing this means leaving money with the government.

What This Means for Your Portfolio

India has 119 million crypto owners — the highest in the world. Most are young salaried professionals, and most are doing it without a plan. A Rs 5,000/month allocation, done consistently through DCA and structured through the right tax vehicle, transforms crypto from speculation into a systematic investment.

Fidelity's research is clear: the cost of a 0% allocation is higher than the risk of a 1-3% allocation. For a salaried Indian, Rs 5,000/month is a practical expression of that insight — large enough to matter over time, small enough to absorb within a monthly budget.

The decision is not just about which asset to buy — it is about which tax structure to buy it through. Spot crypto at 30% flat, derivatives at slab rate, or ETFs at 12.5% LTCG. For salaried employees in the lower tax brackets under the new regime, managed crypto derivatives portfolios offer the combination of professional risk management and the most favourable tax treatment available.

An Option Worth Exploring: Managed Crypto Baskets

For salaried investors who want crypto exposure without the complexity of self-managed DCA, exchange selection, and tax optimisation, managed crypto baskets offer a structured alternative. Grade Capital, for instance, runs a managed crypto derivatives fund with curated baskets — including different baskets that delivered more than 100% profit in the past 12 weeks with a calculated XIRR of more than +75% (12-month holding).

Source: Grade Capital App — Managed crypto baskets with curated portfolios. The app features goal-based investment plans (e.g. Retirement with personalised target amounts), basket selection with calculated XIRR, and lumpsum investment starting at Rs 12,000.

What makes this relevant for salaried investors:

Tax efficiency. Because Grade Capital operates through crypto derivatives (futures and options), gains are taxed as speculative business income under Section 43(5) — at your slab rate, not the flat 30%. For a salaried employee in the lower brackets under the new regime, this could mean 0-5% tax instead of 31.2%.

Professional risk management. The fund uses hedged positions (including options) to deliver returns even in falling markets — something a simple BTC DCA cannot do. The fund's Sharpe ratio of 1.71 (vs Bitcoin's 0.96) reflects this risk-adjusted outperformance, with 25 of 36 months being positive.

Goal-based planning. The app allows salaried investors to set personalised goals — retirement, wealth building, education — with target amounts and XIRR projections. This aligns crypto with the same goal-based framework that mutual fund investors are already familiar with.

Institutional custody. Assets are held through Fireblocks (SOC 2 Type II, ISO 27001 certified), with 80% in cold storage — a level of security that addresses the counterparty risk highlighted by the WazirX incident.

The minimum investment is Rs 12,000 lumpsum — approximately 2.4 months of the Rs 5,000 plan. For a salaried investor who has built a 3-month buffer, this is an accessible entry point. Learn more about managed crypto portfolios on the Grade Capital Knowledge Hub.

Disclaimers

This content is for informational and educational purposes only and does not constitute financial advice or an offer to invest.

Past performance is not indicative of future results. The returns presented are historical and may not be repeated.

Tax treatment depends on individual circumstances and the prevailing interpretation of tax laws. Investors are advised to consult with qualified tax professionals to understand how these provisions apply to their specific situation.

The projections used in this article are illustrative scenarios, not forecasts. Actual returns may vary significantly based on market conditions, timing, and asset selection.

Crypto asset investments are subject to market risks, including the potential loss of entire invested capital. There is no DICGC-equivalent deposit insurance for crypto holdings.