What Is a Crypto ETF? Types, Returns, and What It Means for Indian Investors

A crypto ETF is an exchange-traded fund that tracks the price of one or more cryptocurrencies. It trades on a stock exchange — just like an equity or gold ETF, so investors gain exposure to digital assets without holding tokens, managing private keys, or opening accounts on crypto exchanges.

The instrument is not new in concept. Gold ETFs solved the same problem for precious metals two decades ago. Crypto ETFs do it for Bitcoin, Ethereum, and a growing list of digital assets — with one critical difference: the underlying crypto market trades 24/7 across global exchanges, while the ETF itself trades only during stock exchange hours. This gap creates pricing dislocations at market open, particularly after volatile weekends.

How a Crypto ETF Works

The structure depends on what the fund actually holds. A spot crypto ETF buys and custodies the underlying asset directly. When you buy a share of BlackRock's iShares Bitcoin Trust (IBIT), the fund holds Bitcoin on your behalf. A futures-based crypto ETF, by contrast, holds CME-traded derivative contracts rather than the asset itself.

This distinction matters. Spot ETFs track the actual price of the crypto asset with minimal deviation. Futures ETFs introduce roll costs, the expense of replacing expiring contracts with new ones, which creates tracking error over time. For a long-term holder, the difference compounds.

Both structures are regulated. In the US, spot crypto ETFs fall under SEC oversight. Futures-based products were the first to receive approval, with ProShares BITO launching in October 2021. Spot Bitcoin ETFs followed in January 2024.

The custody arrangement is the other critical difference. A spot crypto ETF requires the fund manager to engage a qualified custodian — typically Coinbase Custody or Fidelity Digital Assets to hold the underlying tokens in segregated cold storage. The investor never interacts with the blockchain. From a portfolio perspective, buying a share of a crypto ETF is operationally identical to buying a share of a gold ETF or an S&P 500 index fund.

The Four Types of Crypto ETF

Not all crypto ETFs serve the same purpose. Four distinct categories exist, each with a different risk-return profile.

Spot crypto ETFs hold the actual digital asset in cold storage through regulated custodians. BlackRock's IBIT and Fidelity's FBTC are the two largest by AUM. These track the real-time price of Bitcoin with near-zero tracking error. For long-term investors seeking passive crypto exposure, spot ETFs are the most efficient vehicle available.

Futures crypto ETFs hold CME-traded contracts instead of the asset. ProShares BITO was the first US-approved Bitcoin ETF of any kind. These are better suited for short-term tactical positions than long-term holding — roll costs erode returns over time. In a contango market, where futures trade above spot, the monthly roll alone can cost 0.5–1.5% of NAV.

Leveraged crypto ETFs use derivatives to amplify daily returns by 2x or 3x. A 2x leveraged Bitcoin ETF aims to deliver twice Bitcoin's daily return. The compounding effect makes these unsuitable for holding periods beyond a single day — a 10% drop followed by a 10% rise does not return to breakeven at 2x exposure. These products exist for day traders, not for investors.

Inverse crypto ETFs profit when the underlying asset declines in price. These are hedging instruments, not investment vehicles. Holding an inverse ETF during a sustained uptrend results in guaranteed capital destruction through daily rebalancing. Portfolio managers use them for short-term risk reduction during specific market events — not as a standalone allocation.

Global Crypto ETF Performance: What the Data Shows

The numbers tell a clear story. As of April 2026, total spot Bitcoin ETF AUM across all 11 US-listed products stands at $96.5 billion. BlackRock's IBIT alone holds 806,700 BTC — valued at approximately $63.7 billion commanding nearly 49% of the entire US spot Bitcoin ETF market.

Spot Ethereum ETFs, approved in July 2024, hold approximately $12.3 billion in AUM. BlackRock's ETHA leads this category with over $6.5 billion. The ten-day consecutive inflow streak of $633 million recorded in April 2026 confirms sustained institutional demand.

The competitive landscape continues to expand. Morgan Stanley launched MSBT in early April 2026, the first spot Bitcoin ETF from a major US bank with the lowest management fee in the market at 0.14%. Fee compression across the category signals that issuers view crypto ETFs as a permanent product line, not a speculative experiment.

Cumulative net inflows into spot Bitcoin ETFs have reached $56.9 billion since launch. These funds now hold roughly 4.7% of Bitcoin's total circulating supply. The combined AUM of spot Bitcoin and Ethereum ETFs approximately $109 billion — exceeds the total AUM of all global silver ETFs.

The inflow pattern has structural implications. During Q1 2026, Bitcoin prices fell by 25%, yet BlackRock's IBIT recorded $8.4 billion in net inflows. Institutional allocators treated the drawdown as an entry point, not an exit signal. This behaviour distinguishes crypto ETF capital from the speculative retail flows that dominated earlier market cycles.

What ETF Approval Does to the Broader Crypto Market

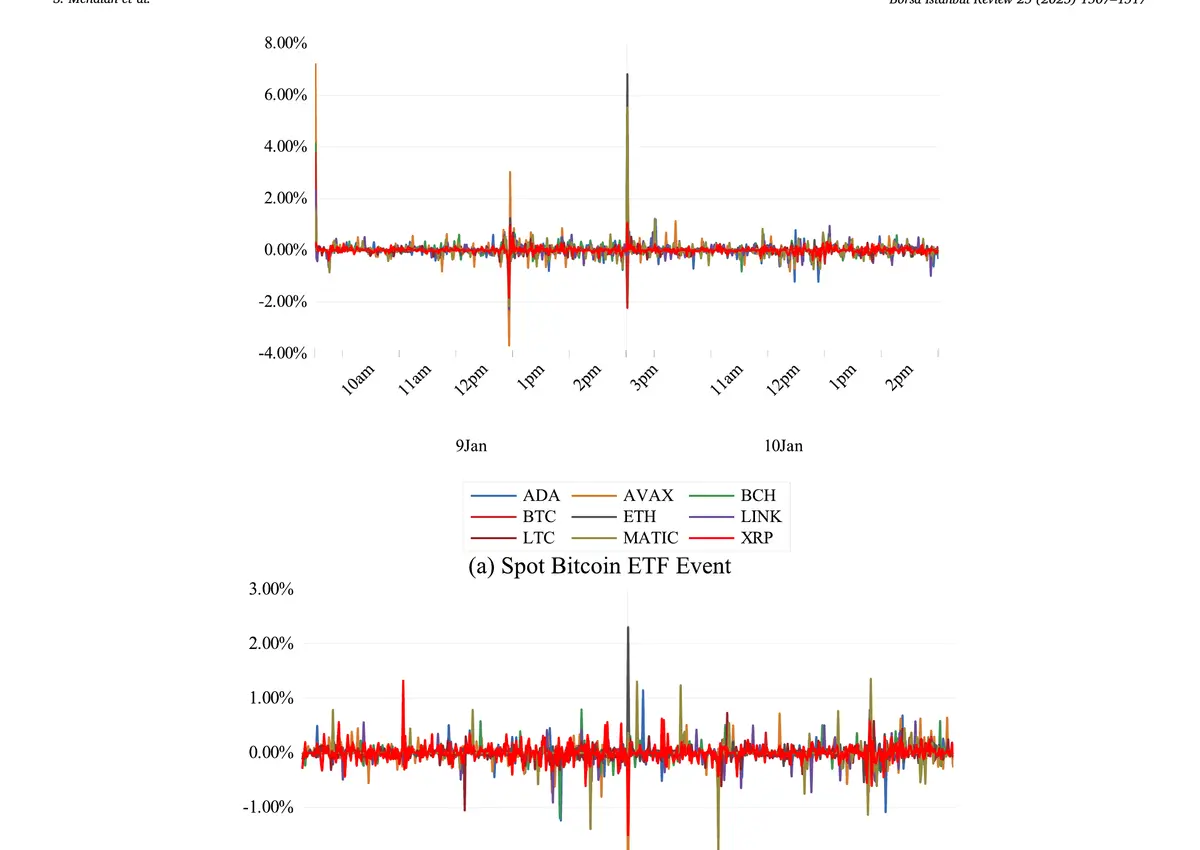

The approval of crypto ETFs does not affect only the underlying asset. Research published in Borsa Istanbul Review by Mehdian, Gherghina, and Stoica (2025) studied the intraday and multi-day impact of both Bitcoin and Ethereum ETF approvals on nine major cryptocurrencies.

The findings are significant. Bitcoin's spot ETF approval in January 2024 triggered a 6.8% intraday volatility spike. Ethereum experienced cumulative abnormal returns (CAR) of 7.87% within the first five trading days. Chainlink's CAR reached 6.27% in the same window.

The market-wide response confirmed that ETF approval functions as a structural catalyst not just for the target asset, but across the ecosystem.

Fig. 1: Intraday price trends of leading cryptocurrencies around Bitcoin and Ethereum ETF approval events. Source: Mehdian, Gherghina & Stoica (2025), Borsa Istanbul Review.

The Ethereum ETF approval in July 2024 produced more modest effects — approximately 3% price movement — suggesting that the market had partially priced in the second approval based on the precedent set by Bitcoin.

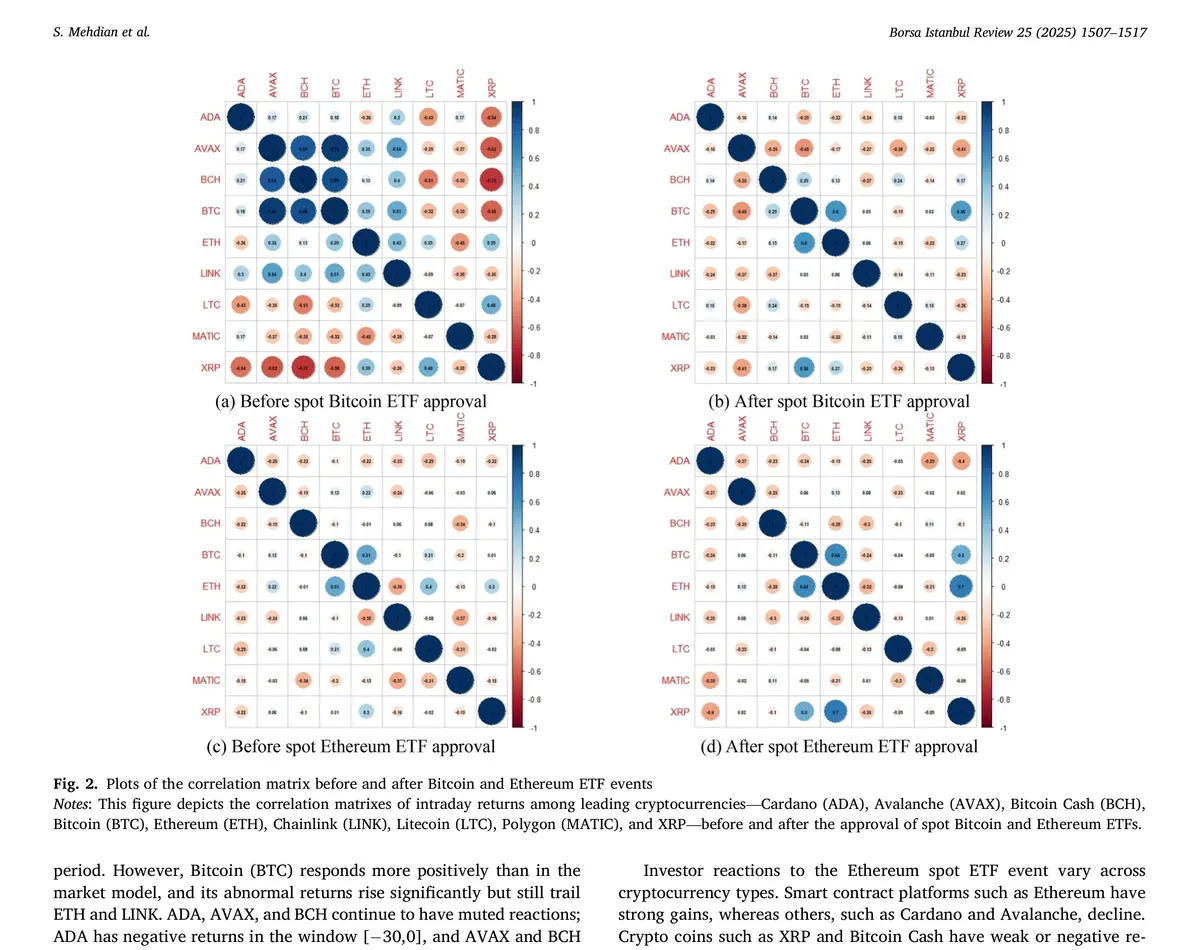

The more consequential finding relates to inter-crypto correlation. Before the Bitcoin ETF approval, the total spillover index across nine major cryptocurrencies stood at 691.82. After approval, it dropped to 403.82 — a 42% reduction. This means crypto assets became less correlated with each other after institutional capital entered through ETFs.

Fig. 2: Correlation matrices of intraday returns among leading cryptocurrencies — before and after Bitcoin and Ethereum ETF approval events. Source: Mehdian, Gherghina & Stoica (2025), Borsa Istanbul Review.

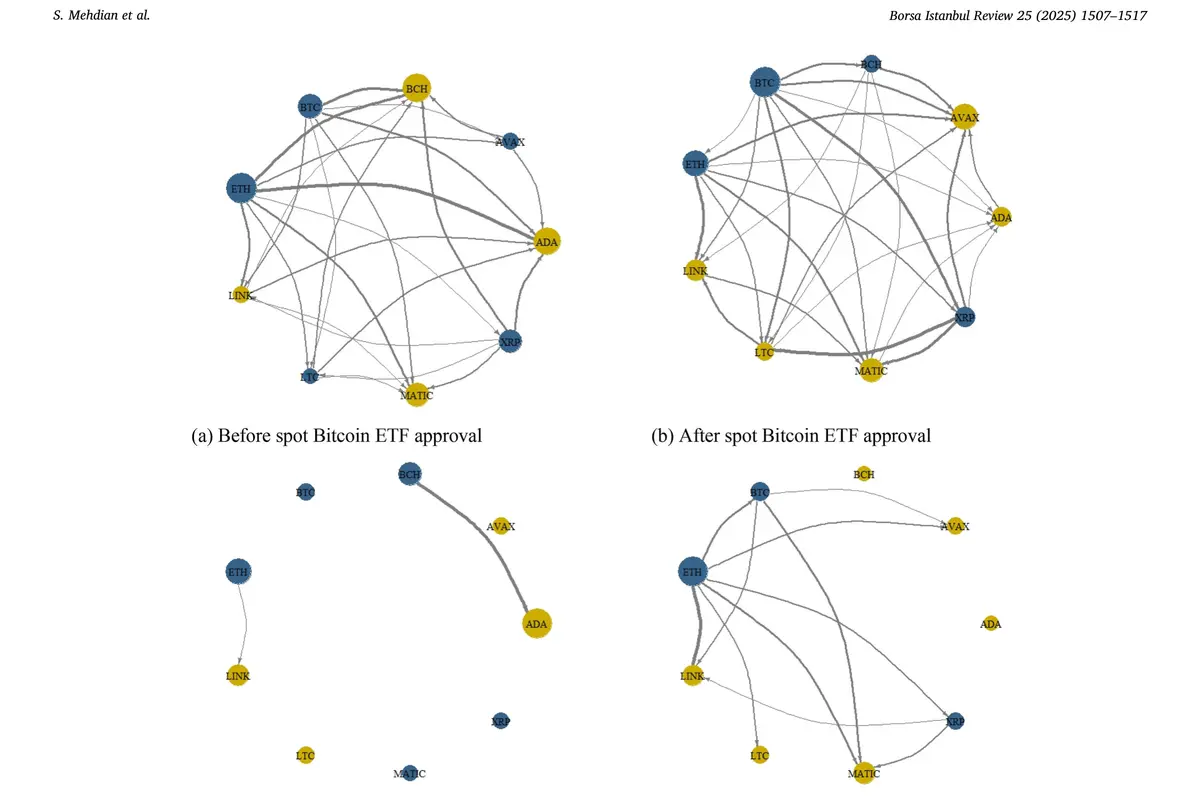

The network connectedness data confirms this pattern. Bitcoin and Ethereum remained the dominant transmitters of market shocks, but the overall network became less dense. Individual assets began trading more independently — a structural shift that improves diversification potential for portfolio managers.

Fig. 3: Network plots of connectedness among leading cryptocurrencies before and after ETF approval events. Blue nodes represent net shock transmitters; yellow nodes represent net shock receivers. Source: Mehdian, Gherghina & Stoica (2025), Borsa Istanbul Review.

The practical implication is clear: crypto ETF approvals reshape market microstructure in ways that benefit long-term, diversified portfolio strategies over concentrated single-asset bets.

Crypto ETF Access for Indian Investors: The Regulatory Reality

No crypto ETF is available on any Indian stock exchange. SEBI has not approved any such product, and mutual funds are explicitly barred from making crypto-related investments until a dedicated law is enacted. The Invesco CoinShares Global Blockchain ETF Fund of Fund — the closest product to receive SEBI approval — was put on hold due to regulatory uncertainty.

Indian residents can, in principle, buy US-listed crypto ETFs like IBIT through the Liberalised Remittance Scheme (LRS). The annual limit is $250,000 per individual. Since these are SEC-regulated ETFs listed on NYSE, they qualify as permissible foreign securities under LRS — distinct from direct crypto purchases, which RBI has blocked from the scheme.

The tax treatment adds friction. Overseas investments exceeding ₹10 lakh in a financial year attract 20% Tax Collected at Source (TCS). The TCS is adjustable against income tax liability, but it creates an upfront cash flow burden.

Capital gains on foreign ETFs held for less than 36 months are taxed at slab rates. Holdings beyond 36 months attract 20% long-term capital gains tax with indexation benefit.

The effective cost stack — LRS processing fees, forex conversion charges, 20% TCS above ₹10 lakh, and foreign brokerage — makes small-ticket crypto ETF investments economically inefficient for most Indian retail investors.

Crypto ETF vs Managed Crypto Portfolio: A Structural Comparison

For Indian investors, the question is not whether crypto ETFs are useful — they are. The question is whether the access route makes sense given the cost structure and regulatory constraints.

A managed crypto derivatives portfolio achieves a similar structural outcome: professionally managed exposure to crypto markets, without the investor needing to trade directly. The difference lies in jurisdiction and strategy. A crypto ETF provides passive exposure to a single asset — Bitcoin or Ethereum. A managed portfolio can deploy active strategies across multiple assets, including derivatives-based approaches like straddle and strangle structures that generate returns in both rising and falling markets.

Grade Capital operates a managed crypto derivatives fund accessible to Indian investors starting at ₹12,000. The fund uses options-based strategies on regulated crypto derivatives, reports daily NAV in USDT. Unlike the LRS route for foreign ETFs, this structure avoids the 20% TCS threshold, forex conversion friction, and the 36-month holding period for favourable tax treatment.

The managed portfolio does not replace a crypto ETF, it addresses the same investor need through a different structure, optimised for the Indian regulatory and tax environment.

The distinction matters for risk management as well. A crypto ETF gives exposure to a single asset's price direction. A managed portfolio can hedge downside through options, generate income through premium selling, and rotate across assets based on market conditions. The Mehdian et al. (2025) research confirms that post-ETF markets reward diversified, strategy-driven approaches over passive single-asset holding.

The Bottom Line

A crypto ETF is the most significant structural development in digital asset investing since the launch of Bitcoin futures on CME in 2017. It brings institutional custody, regulatory oversight, and stock exchange liquidity to an asset class that previously required direct interaction with crypto infrastructure.

For global investors, spot crypto ETFs, particularly Bitcoin — have delivered on their promise. $96.5 billion in AUM and $56.9 billion in cumulative net inflows confirm that institutional capital treats this as a permanent allocation, not a speculative experiment.

Indian investors face a narrower set of options. Until SEBI approves a domestic crypto ETF product, the choice is between navigating LRS constraints for US-listed ETFs or accessing managed crypto strategies that operate within the Indian framework.

The instrument matters less than the outcome it delivers: regulated exposure, professional risk management, and a cost structure that does not erode returns before they begin. For Indian investors allocating ₹1–10 lakh to the crypto asset class, a managed portfolio with no LRS friction, no 20% TCS, and active risk control is a structurally superior route to the same destination. The crypto ETF solved the access problem globally, the next step is solving it within India's regulatory framework.