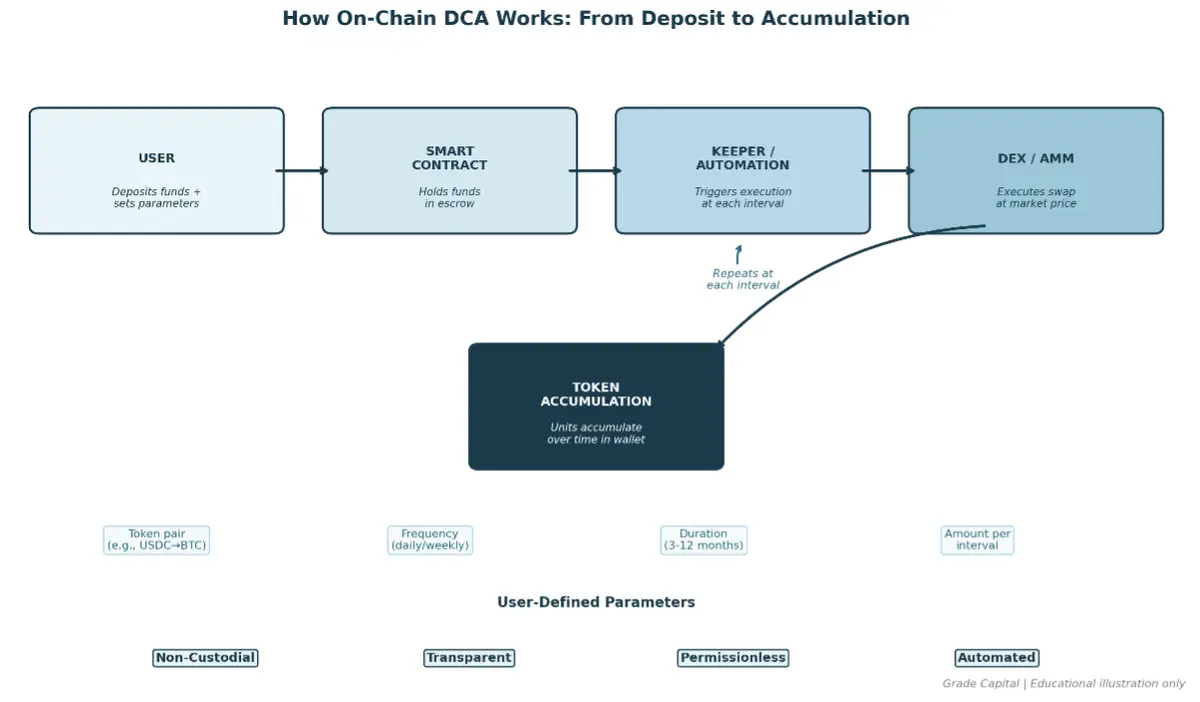

On-chain DCA uses smart contracts to execute recurring cryptocurrency purchases automatically — without any custodial intermediary holding your funds. A user deposits capital into a protocol, defines parameters (which token to buy, how often, how much per interval), and the smart contract handles execution at each period. No exchange account required. No KYC. No counterparty risk from a centralised platform.

This is not theoretical. Protocols like Mean Finance, Bitflow, and Fraxswap have been executing on-chain DCA for thousands of users across Ethereum, Arbitrum, Solana, and Stacks. The DCA bot development market was valued at $55.7 million in 2024 and is projected to reach $115 million by 2031.

Yet on-chain DCA remains a niche activity. The overwhelming majority of systematic crypto investors — including the 572,000+ new SIP users on CoinDCX alone in 2025 — still use centralised exchange products. This article examines why on-chain DCA matters, how it works technically, which protocols offer it, and what the real trade-offs are for Indian investors.

How On-Chain Crypto SIP (DCA) Works: The Technical Architecture

On-chain crypto SIP replaces the centralised exchange's role with three components working together:

1. Smart Contract (Escrow + Logic): Holds user funds and defines the DCA parameters — token pair, amount per interval, frequency, and duration. The contract is permissionless; anyone can deposit and configure a position.

2. Keeper Network (Trigger Mechanism): An off-chain monitoring system (such as Chainlink Automation) watches the blockchain clock and triggers the smart contract to execute each purchase when the interval arrives. Without keepers, someone would need to manually call the contract each period.

3. DEX / AMM (Execution Layer): The actual swap happens on a decentralised exchange — Uniswap, SushiSwap, or the protocol's embedded AMM. The smart contract routes the purchase through available liquidity at market price.

The result: your funds never leave a smart contract you can verify on-chain. No exchange holds custody. No intermediary can freeze, delay, or misappropriate your capital. Each transaction is publicly auditable on the blockchain.

Figure 1: How on-chain DCA works — from user deposit through smart contract execution to token accumulation. Educational illustration.

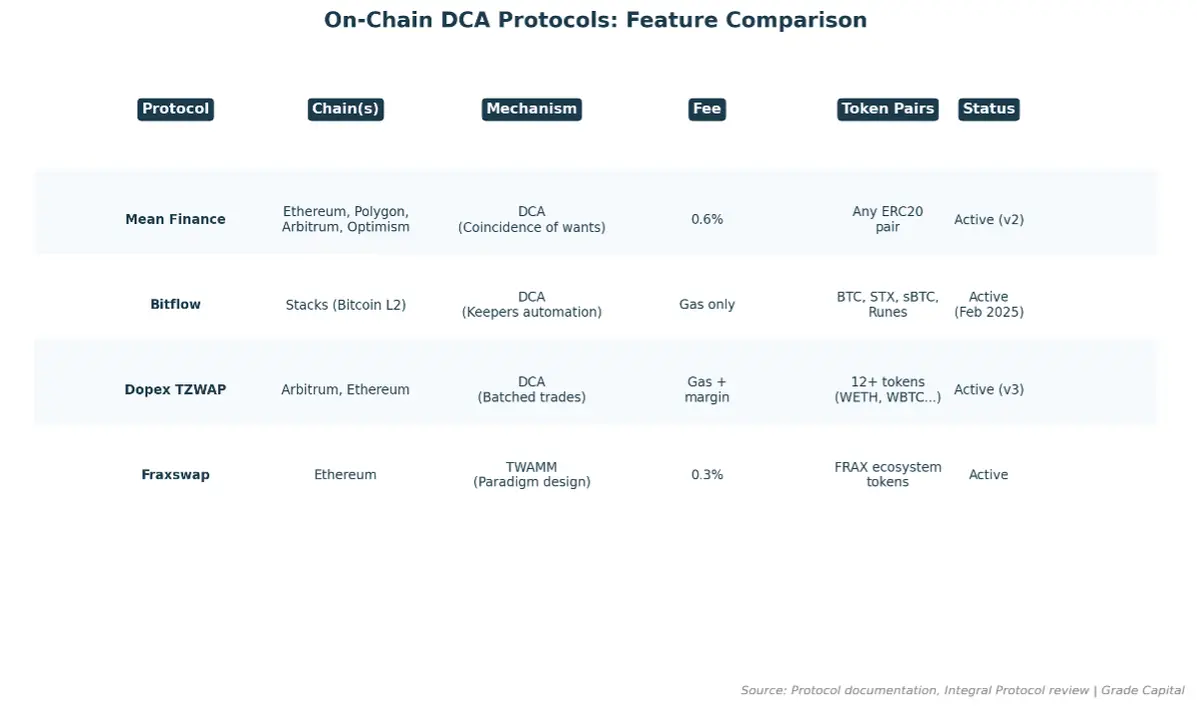

Key On-Chain DCA Protocols in 2025-2026

Several protocols have built functional on-chain DCA infrastructure. Each takes a different architectural approach.

Mean Finance: Any ERC20 Pair, NFT Positions

Mean Finance is an open protocol enabling DCA between any two ERC20 tokens on Ethereum, Polygon, Arbitrum, and Optimism. Users deposit capital, specify the DCA parameters, and receive an NFT representing their position. This NFT is transferable — you can sell or delegate your DCA position.

Trades are matched via coincidence of wants between users (if someone is DCA-ing from USDC to ETH while another goes ETH to USDC, they offset) or executed by external market makers. Fee: 0.6% per swap. The protocol was paused briefly after a responsible bug disclosure through ImmuneFi — no user funds were lost — and relaunched as v2.

Bitflow: Bitcoin DCA on Stacks

Launched in February 2025, Bitflow brings automated DCA to Bitcoin's ecosystem via the Stacks Layer 2 network. Users can set recurring purchases of BTC, sBTC, STX, and Runes tokens. The system is powered by Bitflow Keepers — a smart automation engine that triggers purchases without custodial intermediaries.

Key differentiator: this is DCA for Bitcoin specifically, not just EVM tokens. It supports SIP-10 tokens and Runes assets, operating fully on-chain with non-custodial execution.

Fraxswap: TWAMM-Based Execution

Fraxswap implements the TWAMM (Time-Weighted Automated Market Maker) concept proposed by Paradigm researchers Dave White, Dan Robinson, and Hayden Adams in 2021. The TWAMM breaks long-term orders into infinitely many infinitely small virtual sub-orders, executed smoothly over time against an embedded constant-product AMM.

The mathematical elegance: rather than executing discrete purchases at intervals (which are predictable and exploitable), TWAMM executes continuously. This makes the execution resistant to sandwich attacks and front-running. Fee: 0.3%. Currently limited to Frax ecosystem tokens.

Dopex TZWAP: Batched DCA on Arbitrum

Dopex, primarily an options protocol, offers TZWAP — a batched execution system where traders specify a total amount, batch size (as percentage), and time delay between batches. A 100 ETH sell could execute as 5% every 5 minutes. Supports 12+ tokens across Arbitrum and Ethereum mainnet. Now on its third iteration.

Figure 2: On-chain DCA protocol comparison — chains, mechanisms, fees, and token support. Source: Protocol documentation.

Protocol | Chain(s) | Mechanism | Fee | Key Feature |

Mean Finance | ETH, Polygon, Arb, OP | Coincidence of wants + MM | 0.6% | Any ERC20 pair, NFT positions |

Bitflow | Stacks (Bitcoin L2) | Keepers automation | Gas only | Bitcoin-native DCA |

Fraxswap | Ethereum | TWAMM (Paradigm) | 0.3% | MEV-resistant continuous execution |

Dopex TZWAP | Arbitrum, Ethereum | Batched trades | Gas + margin | Configurable batch size/timing |

Table 1: On-Chain DCA Protocols — Feature Comparison (May 2026)

On-Chain DCA vs Centralised Exchange DCA: The Trade-Offs

The choice between on-chain and exchange-based DCA is not about which is better. It is about which set of trade-offs aligns with your priorities.

Dimension | Centralised Exchange DCA | On-Chain DCA (DeFi) |

Custody | Exchange holds your funds | You hold your keys (non-custodial) |

Transparency | Off-chain execution, trust required | On-chain, fully verifiable |

Setup complexity | One-click, beginner-friendly | Wallet + gas + token approvals |

Fees | Spread + platform fee (predictable) | Gas + protocol fee (variable, network-dependent) |

MEV protection | None (exchange controls execution) | TWAMM/batch designs resist MEV |

Token availability | Platform-listed tokens only | Any ERC20 (Mean Finance) or chain-native |

Regulatory status (India) | FIU-registered, KYC/AML compliant | Grey area under PMLA; no FIU registration |

Primary risk | Exchange insolvency or hack | Smart contract exploit |

Automation | Fully automated by exchange | Requires keeper network infrastructure |

Table 2: On-Chain DCA vs Centralised Exchange DCA — Full Trade-Off Comparison

Figure 3: On-chain vs centralised exchange DCA — the key trade-offs at a glance. Grade Capital.

The Real Risks of On-Chain DCA

On-chain DCA is not risk-free. It trades one set of risks (custodial, counterparty) for another (technical, economic). The distinction matters.

Smart Contract Risk

DeFi smart contract vulnerabilities caused over $3.1 billion in losses from 2023 to 2025. SlowMist reported 200 DeFi protocol hacks in 2025 alone, totalling $2.9 billion — a 40% increase over 2024. Flash loan attacks accounted for 83.3% of exploits. Your DCA position is only as safe as the smart contract it sits in.

Mean Finance itself was paused after a vulnerability disclosure. No funds were lost, but the incident illustrates that even audited protocols carry residual risk. Unlike centralised platforms that may offer partial insurance or recovery, a smart contract exploit typically means permanent loss.

Gas Cost Erosion

Every periodic purchase incurs a blockchain transaction fee. On Ethereum mainnet, this can be $5-50+ per transaction depending on network congestion. For a monthly DCA of $100, a $20 gas fee represents a 20% drag on returns — a cost that never recovers.

Mitigations exist: Layer 2 deployment (Arbitrum gas: $0.01-0.10), batch execution across users (socialising costs), and longer intervals (weekly/monthly instead of daily). But gas remains a structural friction that centralised exchanges do not impose.

Oracle and Price Feed Manipulation

DCA protocols that rely on external price oracles (for TWAP calculations or slippage protection) are vulnerable to oracle manipulation. In 2024, price manipulation accounted for 18 exploit incidents. If an attacker manipulates the price feed during your DCA execution window, you receive fewer tokens than the fair market rate.

Liquidity Risk

On-chain DCA executes against DEX liquidity pools. For major pairs (ETH/USDC, BTC/USDT), this is rarely an issue. But for long-tail tokens, thin liquidity means significant slippage on each purchase — a hidden cost that compounds over dozens of intervals.

Regulatory Uncertainty (India)

India's PMLA VASP Notification covers five activities including exchange of VDAs and transfer of VDAs. DeFi protocols operate in a regulatory grey area — the notification does not expressly distinguish between centralised and decentralised platforms. The legal position: a 'mere self-claim of being decentralised is insufficient' for regulatory exemption. Indian investors using on-chain DCA should understand this ambiguity.

Tax Treatment: On-Chain DCA Under Indian Law

From a tax perspective, on-chain DCA does not change the fundamental treatment. Each swap executed by the smart contract creates a separate taxable event under Section 115BBH:

· Each periodic purchase = separate acquisition with its own cost basis

· Gains taxed at flat 30% with no loss offset or carry-forward

· 1% TDS applies on each transaction above threshold (though enforcement on DeFi swaps remains unclear)

· The smart contract does not withhold or report TDS — compliance burden falls entirely on the investor

An alternative structure: crypto derivatives are taxed as speculative business income under Section 43(5) — slab rates, expense deductions, and loss carry-forward. Professionally managed portfolios like those offered by platforms such as Grade Capital operate within this derivatives framework, avoiding the 30% flat VDA tax entirely.

Tax treatment depends on individual circumstances and the prevailing interpretation of tax laws. Investors are advised to consult with qualified tax professionals to understand how these provisions apply to their specific situation.