Institutional investors’ digital asset allocation is no longer a question of if. It is a question of how much, through which vehicles, and at what pace. In the 2025 EY-Parthenon and Coinbase survey of 352 institutional investors, 83% reported plans to increase their crypto allocations — and 85% had already increased allocations during 2024. BlackRock’s iShares Bitcoin Trust alone holds $63.5 billion in assets. The structural shift is underway.

What has changed is not sentiment — institutional curiosity has existed for years. What has changed is infrastructure. Regulated ETFs, institutional-grade custody, tokenized money markets, and clearer regulatory frameworks have collectively removed the barriers that kept allocation committees on the sidelines.

The Survey Evidence: Allocation Intent Across Four Major Studies

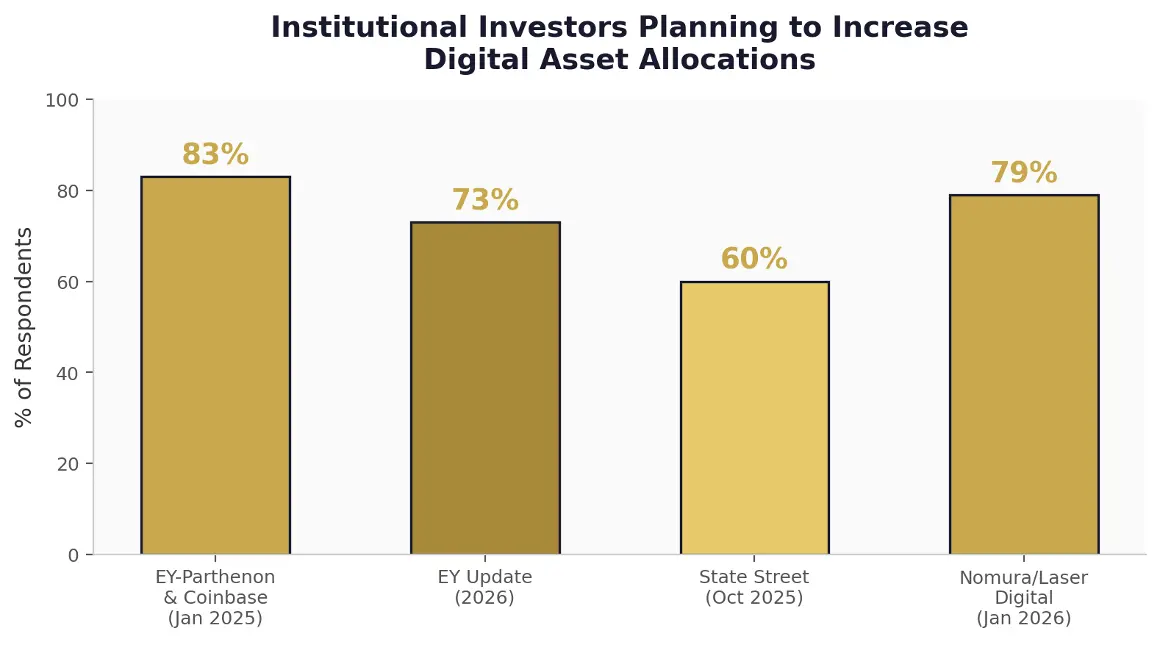

Four major institutional surveys, conducted independently across different geographies and investor types, converge on the same conclusion: the majority of institutional investors are increasing their digital asset exposure. The respondent pools span 352 to 518 participants across the US, Europe, and Japan — asset managers, hedge funds, pension funds, family offices, and insurance companies.

Figure 1: Percentage of institutional investors planning to increase digital asset allocations. Sources: EY-Parthenon/Coinbase (2025), EY (2026), State Street (2025), Nomura/Laser Digital (2026).

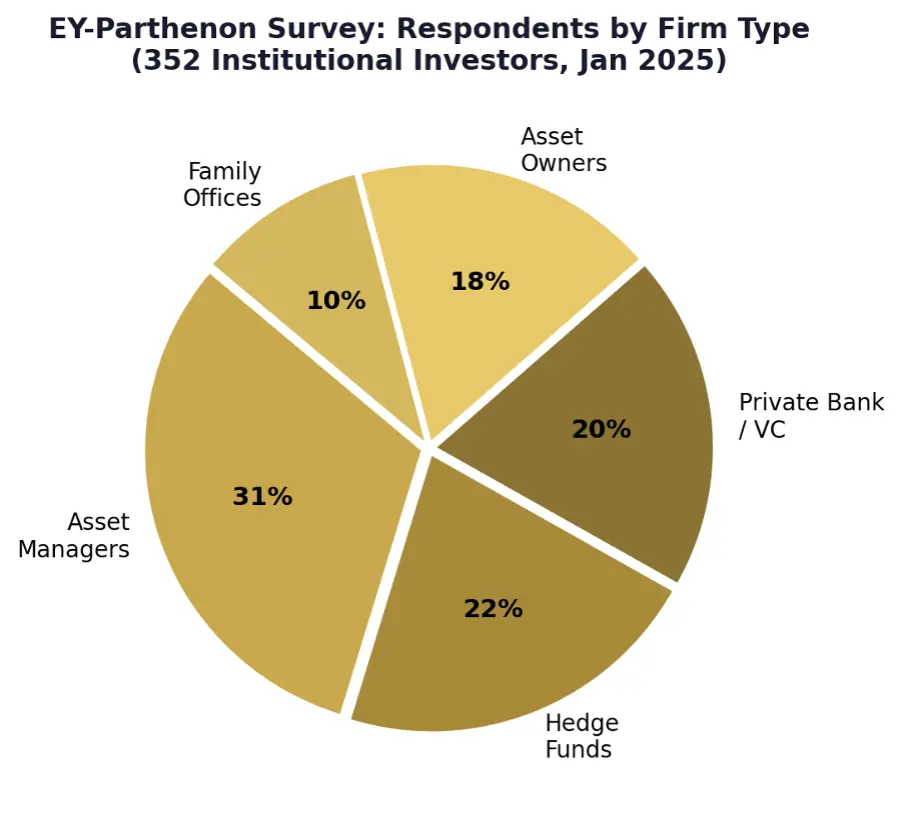

The EY-Parthenon and Coinbase survey (January 2025, 352 respondents) provides the most granular view. The respondent pool comprised 32% asset managers, 22% hedge funds, 20% private banks and venture capital firms, 18% asset owners, and 10% family offices. Of these, 59% plan to allocate over 5% of AUM to digital assets. 86% either have current exposure or plan allocations within the year. The survey was conducted post-election but prior to the digital asset executive order — meaning the results reflect structural conviction, not policy euphoria. 68% identified digital assets as the biggest risk-adjusted return opportunity in the market.

Figure 2: EY-Parthenon & Coinbase survey respondent breakdown by firm type (352 institutions, January 2025).

The State Street survey (October 2025, 324 respondents) reported that the average institutional portfolio allocation to digital assets stands at 7%, with target allocations expected to rise to 16% within three years. A critical nuance: over 50% of respondents currently have less than 1% exposure — indicating that while intent is high, actual deployment remains early-stage for the majority. By 2030, 52% expect that 10–24% of all investments will be made via digital assets or tokenized instruments. 40% of respondents have established dedicated digital asset teams within their organisations.

The Nomura and Laser Digital survey (January 2026, 518 investment professionals in Japan) found that 65% view crypto as a portfolio diversifier alongside traditional holdings. The respondent pool spanned banks (19%), life insurance companies (13%), family offices (13%), pension funds (8%), and asset managers (8%). Among respondents with high knowledge of digital assets, 58% hold a positive view. 55% intend to invest immediately or within the next year, with 60% expecting to allocate 2–5% of total portfolio. Positive sentiment rose to 31%, up 6 percentage points from 2024.

The EY 2026 update confirmed continued momentum: 73% plan to increase allocations, though institutions are approaching growth more deliberately than in prior years — prioritising repeatable access models and clearer risk guardrails around liquidity, position sizing, and governance.

The convergence across these four surveys — conducted independently, across different geographies, with different respondent pools — is itself a data point. When 60–83% of institutional investors across the US, Europe, and Japan report the same directional intent, the signal is structural, not anecdotal. The question has shifted from whether institutions will allocate to digital assets to how quickly their internal governance and compliance frameworks can process the decision.

Why Institutions Are Allocating: The Investment Thesis

The rationale for institutional crypto allocation has matured beyond speculative upside. The EY-Parthenon survey found that 59% cite higher expected returns as the primary motivation, but the Nomura data tells a more nuanced story: 50% of Japanese institutional respondents identify portfolio diversification as the top reason, followed by low correlation with traditional assets (35%).

The State Street survey adds a structural dimension. Institutions are not merely buying crypto for price appreciation — they are integrating digital assets into their operational infrastructure. 52% cite increased transparency as the primary benefit of tokenization. 39% cite faster trading. 32% cite lower compliance costs. These are infrastructure arguments, not speculation arguments.

This shift in investment thesis is significant. In 2021–2022, institutional interest was largely driven by fear of missing out on a rapidly appreciating asset class. In 2025–2026, the thesis has matured to portfolio construction fundamentals: diversification, low correlation, and operational efficiency through tokenized infrastructure. The EY survey found that 79% of institutional respondents expect crypto prices to rise — but the allocation decisions are being made on structural grounds, not price predictions.

The ETF Gateway: How Institutions Are Getting In

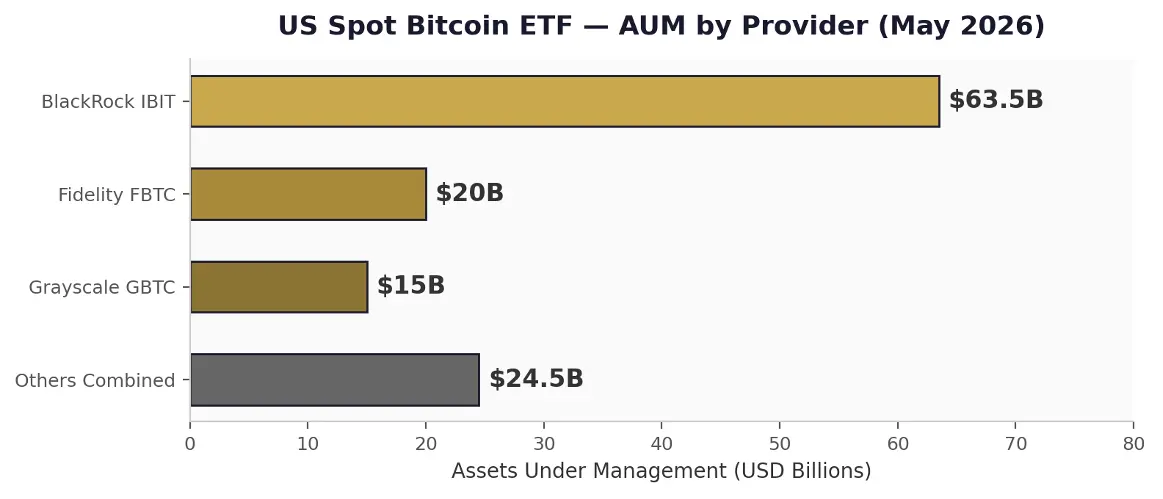

Figure 3: US Spot Bitcoin ETF assets under management by provider (May 2026). Source: iShares, public ETF data.

Exchange-traded products have become the dominant entry point for institutional digital asset exposure. The numbers confirm this decisively.

US spot Bitcoin ETFs collectively manage over $123 billion in assets. BlackRock, Fidelity, and Grayscale control more than 85% of this market. BlackRock’s IBIT alone commands approximately 49% market share with $63.5 billion in net assets.

The scale of institutional commitment is visible in the flow data. IBIT attracted over $25 billion in investor capital during 2025 — ranking sixth among all ETFs by inflows, not just crypto ETFs. In Q1 2026, BlackRock reported $935 million in net digital asset inflows during a quarter where crypto prices fell. Positive inflows during a price decline is a structural signal, not a speculative one.

The preference for regulated vehicles is accelerating. 81% of institutions now prefer spot exposure through a registered vehicle such as an ETF — up from 60% in 2025, according to the EY-Parthenon data. BlackRock’s European Bitcoin ETP (IB1T), launched in March 2025, surpassed $1.1 billion in AUM within its first year, confirming that institutional demand extends beyond US borders.

Grayscale’s 2026 outlook identifies a critical observation: the maximum year-over-year Bitcoin price increase was approximately 240% (in the year to March 2024), reflecting steadier institutional buying compared to the retail momentum chasing that characterised earlier cycles. The firm expects this pattern to mark the end of the so-called four-year cycle — the theory that crypto market direction follows a recurring pattern tied to Bitcoin halvings. Institutional capital, by its nature, does not operate on halving schedules. It operates on allocation committee timelines, compliance approvals, and fiduciary mandates.

Pension Funds and Endowments: The 13F Evidence

Survey data captures intent. SEC 13F filings capture action. David Krause’s SSRN research analysed 15 pension funds and 5 endowments across 382 institution-quarter-security observations from Q1 2024 through Q4 2025 — providing the most granular view of how conservative institutional capital is entering digital assets.

Aggregate institutional crypto holdings grew from $450.2 million in Q1 2024 to a peak of $1,478.8 million in Q3 2025 — a 229% increase in 18 months. The Q4 2025 drawdown reduced holdings to $965.5 million, a 34.7% decline from peak.

The data reveals critical behavioural differences between institution types. Pension funds concentrated 58.4% of their aggregate crypto holdings in MicroStrategy (MSTR) — an indirect Bitcoin proxy — rather than direct spot ETFs. Endowments, by contrast, allocated exclusively through spot ETFs (IBIT, FBTC, ETHA). This divergence reflects differing governance structures: pension funds may find it easier to justify a publicly traded equity (MSTR) to investment committees than a novel ETF wrapper, while endowments — with longer time horizons and fewer regulatory constraints — moved directly into spot crypto vehicles.

During the Q4 2025 drawdown, pension funds declined 43.0% versus endowments declining 18.8%, suggesting endowments have higher conviction and longer time horizons for digital assets. Harvard Management Company’s allocation reached 0.84% of AUM. The divergence in drawdown response between institution types is itself instructive for portfolio construction.

Notable Institutional Positions (13F Data)

Institution | Type | Primary Vehicle | Notable Detail |

Wisconsin SWIB | Pension Fund | IBIT (6.06M shares) | $321.5M — largest single position |

CalPERS | Pension Fund | MSTR, IBIT | Largest US public pension fund |

Harvard Mgmt Co. | Endowment | IBIT + ETHA rotation | 0.84% of AUM; first crypto rotation in 13F data |

Stanford Mgmt Co. | Endowment | IBIT, FBTC | Multi-ETF diversification approach |

State of Michigan | Pension Fund | IBIT + ETHA | Early public pension adopter |

UTIMCO (Univ. of Texas) | Endowment | Bitcoin direct | Disclosed 2024; direct custody |

Harvard’s simultaneous reduction of IBIT and initiation of an 86.8 million ETHA (Ethereum ETF) position in Q4 2025 represents the first major intra-crypto portfolio rotation documented in 13F data. It signals a shift from single-asset exposure to multi-asset digital allocation at the endowment level.

Beyond ETFs: Tokenization and On-Chain Allocation

ETFs are the entry point. Tokenization is the next frontier. Institutional capital is flowing into tokenized real-world assets — treasury bills, money market funds, private equity, and fixed income — at a pace that was theoretical two years ago.

Metric | Value | Source |

Tokenized RWA total market | $27.6 billion (April 2026) | RWA.xyz / SpazioCrypto |

BlackRock BUIDL fund AUM | $1.9 billion | BlackRock |

JPMorgan Onyx tokenized repo | $900 billion processed | JPMorgan |

RWA market growth (2022–2025) | 380% ($5B to $24B) | Industry data |

BIS projection: tokenized GDP by 2034 | 10% of global GDP | Bank for International Settlements |

Institutions planning tokenized asset investment | 76% by 2026 | EY-Parthenon & Coinbase |

The EY-Parthenon survey found that 76% of institutional investors intend to invest in tokenized assets by 2026 — a figure that underscores the convergence between crypto allocation and traditional asset infrastructure. BlackRock’s BUIDL fund — the USD Institutional Digital Liquidity Fund — crossed $1 billion in AUM in March 2025 and now stands at $1.9 billion. It was approved as off-exchange collateral at a major venue, bridging traditional derivatives markets with on-chain assets.

The State Street data identifies which asset classes institutions expect to tokenize first: private equity leads at 63%, followed by private fixed income at 53%. 50% of respondents believe mainstream tokenization will arrive within four years. The perceived benefits — increased transparency (52%), faster trading (39%), and lower compliance costs (32%) — are operational, not speculative.

JPMorgan’s Onyx platform has processed over $900 billion in tokenized repo transactions. Citi, HSBC, and Goldman Sachs have launched or announced tokenization pilots for bonds, trade finance, and private equity. The BIS projects that 10% of global GDP could be tokenized by 2034.

The distinction between crypto ETF allocation and tokenised asset allocation is important. ETFs provide exposure to the price of digital assets. Tokenisation transforms the infrastructure of traditional assets — bonds, real estate, private equity — by moving them on-chain. Institutional capital is flowing into both simultaneously, but for different strategic reasons. The ETF allocation is a portfolio diversification decision. The tokenisation adoption is an operational efficiency decision. Both represent structural commitment to digital asset infrastructure.

Stablecoins and DeFi: The Emerging Allocation Layer

Stablecoins are no longer a niche instrument. They are becoming an institutional cash management tool. The EY-Coinbase survey found that 84% of institutional investors are either using stablecoins or are interested in doing so.

DeFi engagement is expected to triple. The 2025 EY-Parthenon survey reported 24% of institutions currently engaged with DeFi protocols — this is expected to reach 75% within two years. The Nomura survey found that over 60% of Japanese institutional respondents expressed interest in staking, lending, derivatives, and tokenized assets.

The regulatory backdrop supports this trajectory. The GENIUS Act, passed by Congress in 2025, established a framework for stablecoin issuance. Grayscale’s 2026 outlook identifies stablecoins, DeFi lending, and staking as three of its ten core investing themes for the year.

The Nomura survey reinforces this from the Asian institutional perspective. 63% of Japanese institutional respondents identified potential use cases for stablecoins across treasury management, cross-border payments, crypto investment, and tokenised securities. Stablecoins issued by major financial institutions received the highest trust scores — a clear signal that institutional adoption of DeFi infrastructure follows the same pattern as ETF adoption: regulated access first, direct participation second.

What Keeps Institutions Cautious

The shift is real. It is not without friction. The EY-Coinbase survey identified regulatory uncertainty (52%), volatility (47%), and secure custody (33%) as the top three institutional concerns. The State Street survey adds two further barriers: safety and soundness concerns (46%) and regulatory clarity (43%).

Barrier | EY-Parthenon | State Street | Nomura |

Regulatory uncertainty | 52% | 43% | — |

Volatility / risk | 47% | — | Cited as top concern |

Safety & soundness | — | 46% | — |

Custody concerns | 33% | — | — |

Lack of analysis frameworks | — | — | Specific to Japan |

Counterparty / fraud risk | — | — | Specific to Japan |

Table: Top institutional barriers to digital asset allocation across three major surveys.

The 13F data provides a quantitative view of this caution. The Q4 2025 drawdown — a 34.7% decline in aggregate institutional crypto holdings — demonstrates that even committed allocators reduce exposure during volatility. Pension funds, with their fiduciary obligations and conservative mandates, pulled back more sharply (43.0%) than endowments (18.8%). The Nomura survey adds two barriers specific to Asian institutions: the lack of established frameworks for fundamental analysis, and counterparty risks including default, fraud, and asset loss.

The EY 2026 update captures the evolving institutional posture precisely: enthusiasm is high, but institutions are prioritising repeatable access models and risk guardrails — liquidity management, position sizing discipline, and governance frameworks — over speed of deployment.

What This Means for Individual Investors

Institutional adoption does not guarantee returns. It does confirm that digital assets have passed the credibility threshold for the most conservative pools of capital on the planet — pension funds managing retirement savings, endowments funding universities, and sovereign wealth funds managing national reserves.

The practical implications are structural. As institutional capital enters through regulated vehicles like ETFs and tokenized instruments, the market’s liquidity profile improves, volatility patterns shift, and the infrastructure available to all investors — including retail — becomes more robust.

Managed crypto portfolio strategies, including those offered by platforms like Grade Capital, benefit directly from this institutional infrastructure. Professional custody solutions like Fireblocks, derivatives markets with deep institutional liquidity, and regulated on/off-ramp services — these exist because institutional demand created them. Individual investors who access crypto through managed, professionally structured products inherit the same infrastructure advantages.

The era of institutional digital asset allocation is not arriving. Based on the survey evidence, the ETF flow data, and the 13F filings — it has arrived. The capital is moving. The infrastructure is in place. The remaining question for most investors is not whether to allocate, but how.

Past performance is not indicative of future results. This content is for informational and educational purposes only and does not constitute financial advice or an offer to invest.