The Indian government collected ₹511.83 crore in TDS on cryptocurrency transactions in FY 2024–25, a 41% increase over the previous year. It issued over 44,000 notices to traders who failed to disclose crypto gains. It uncovered ₹888.82 crore in unreported income through search and seizure operations. And in April 2026, it began issuing Section 148A reassessment notices to crypto investors for transactions dating back to FY 2021–22.

The enforcement apparatus is no longer theoretical. The Income Tax Department has the data, the legal authority, and the operational machinery to pursue non-compliant crypto investors. This article maps the full spectrum of consequences, from interest charges to imprisonment — for failing to pay crypto tax in India.

The Tax Framework: What You Owe

Before examining the penalties, the tax obligation itself needs to be clear. Two provisions govern crypto taxation in India.

Section 115BBH imposes a flat 30% tax on income from the transfer of any virtual digital asset (VDA). This rate applies regardless of the taxpayer’s income slab, holding period, or the type of VDA — Bitcoin, Ethereum, NFTs, stablecoins, or any other token. A 4% health and education cess applies on top, bringing the effective rate to 31.2%. Surcharge may further increase this for higher income brackets.

Section 194S requires a 1% tax deducted at source (TDS) on all VDA transfers exceeding ₹10,000 in a financial year (₹50,000 for specified persons). The buyer or the exchange deducts this at the point of transaction. This TDS is not a separate tax — it is an advance payment toward the 30% liability. But it creates a paper trail that the Income Tax Department uses to track every transaction.

Critical restriction: Losses from one VDA cannot be set off against gains from another VDA, or against any other head of income. Losses cannot be carried forward. Infrastructure costs (electricity, hardware) are not deductible. The only deduction permitted is the cost of acquisition of the specific asset being transferred.

Component | Rate / Rule | Section |

Flat tax on VDA gains | 30% (+ 4% cess = 31.2%) | 115BBH |

TDS on VDA transfers | 1% above ₹10,000/year | 194S |

Loss set-off | Not permitted against any income | 115BBH(2) |

Loss carry-forward | Not permitted | 115BBH(2) |

Deductions allowed | Cost of acquisition only | 115BBH(1) |

Gifts of VDA | Taxable in hands of recipient | 56(2)(x) |

Layer 1: Interest Charges

The first layer of consequence is automatic. It requires no investigation, no audit, and no discretion from the assessing officer. If you owe crypto tax and don’t pay it on time, interest accrues at 1% per month under three separate provisions.

Section | Trigger | Rate | Period |

234A | Late filing of ITR | 1% per month | From due date to actual filing date |

234B | Failure to pay advance tax (or paying < 90%) | 1% per month | From April 1 of next FY to date of assessment |

234C | Shortfall in quarterly advance tax instalments | 1% per month | Per instalment shortfall period |

These three interest provisions can apply simultaneously. A trader who earns ₹10 lakh in crypto gains, files late, and fails to pay advance tax faces compounding interest charges from multiple directions. At 1% per month, a one-year delay on a ₹3.12 lakh tax liability (30% + cess on ₹10 lakh) generates approximately ₹37,440 in interest alone.

Any part of a month counts as a full month. The interest is simple, not compound, but it accrues from the original due date — not from the date of discovery. For advance tax under Section 234B, the clock starts from April 1 of the assessment year.

Note: The Income Tax Act, 2025 renumbers these sections as 423, 424, 425, and 426 respectively. The substance and rates remain unchanged.

Layer 2: Penalties for Under-reporting and Misreporting

Interest is the cost of delay. Penalties are the cost of concealment. Section 270A distinguishes between two categories of non-compliance, and the difference in severity is substantial.

Category | Definition | Penalty | Example on ₹10L income |

Under-reporting | Income not declared but no deliberate attempt to mislead | 50% of tax on under-reported amount | ₹1,56,000 |

Misreporting | Deliberate concealment, false entries, fabricated deductions, failure to record investments | 200% of tax on misreported amount | ₹6,24,000 |

The distinction matters. Under-reporting applies when you earn crypto income and simply don’t declare it. Misreporting applies when you actively conceal — for example, by claiming fictitious deductions, recording a false cost of acquisition, or failing to record a VDA investment in your books. The Income Tax Act treats misreporting as a form of fraud, and the penalty reflects this.

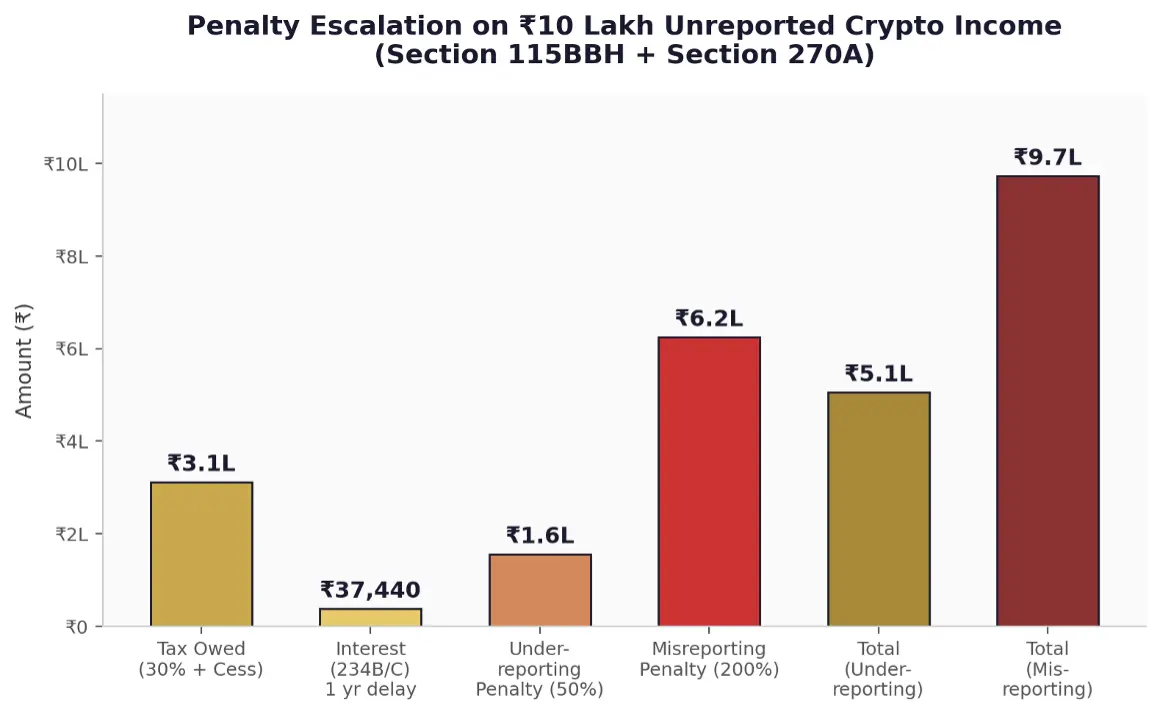

Figure 1: Penalty escalation on ₹10 lakh unreported crypto income. Under-reporting (50% penalty) vs. misreporting (200% penalty), inclusive of tax and 1-year interest.

The math on ₹10 lakh in unreported crypto income:

Component | Under-reporting | Misreporting |

Tax owed (31.2%) | ₹3,12,000 | ₹3,12,000 |

Interest — 1 year (234B/C) | ₹37,440 | ₹37,440 |

Penalty (Section 270A) | ₹1,56,000 (50%) | ₹6,24,000 (200%) |

Total liability | ₹5,05,440 | ₹9,73,440 |

Effective tax rate | 50.5% | 97.3% |

Table: Total liability on ₹10 lakh unreported crypto income with one year of delay. Surcharge not included.

On ₹10 lakh of unreported gains, the effective tax rate rises from 31.2% (if paid on time) to 50.5% for under-reporting or 97.3% for misreporting. At the misreporting level, the government recovers nearly the entire gain.

Section 271AAC imposes an additional 10% penalty on unexplained income under Section 68/69/69A/69B/69C/69D. If the Income Tax Department discovers crypto holdings or income that you cannot explain with legitimate sources, the income is taxed at 60% under Section 115BBE, plus a 25% surcharge and 4% cess effectively 78% — and a further 10% penalty under Section 271AAC. This provision is typically triggered during search and seizure operations.

Layer 3: Criminal Prosecution

The most severe consequence is criminal prosecution. This is not a theoretical risk — 29 individuals have been arrested and 22 prosecution complaints filed in crypto-related enforcement actions, per government data presented to Parliament in December 2025.

Section | Offence | Imprisonment | Threshold |

276C(1) | Wilful attempt to evade tax | 6 months to 7 years + fine | Evaded amount > ₹25 lakh |

276C(1) | Wilful attempt to evade tax | 3 months to 2 years + fine | Evaded amount ≤ ₹25 lakh |

276C(2) | Wilful attempt to evade payment of tax | 3 months to 2 years + fine | Any amount |

277 | False statement in verification | 6 months to 7 years + fine | Tax sought to evade > ₹25 lakh |

276B | Failure to pay TDS to government | 3 months to 7 years + fine | Any amount under Section 194S |

Prosecution requires proof of wilful intent. A genuine mistake in tax calculation, corrected through a revised or updated return, is unlikely to trigger criminal proceedings. But deliberately not reporting crypto income, filing returns with false figures, or operating through unregistered exchanges to avoid the TDS trail, these constitute wilful evasion.

The Supreme Court has clarified that Section 276C(1) targets wilful attempts to evade liability, not mere failure to disclose. Mens rea — criminal intent — must be established. However, the bar for establishing intent is lower than most taxpayers assume. The Income Tax Department’s data analytics systems now cross-reference exchange TDS filings (Form 26QE) with individual ITRs. If an exchange deducted 1% TDS on your transaction but your ITR shows no VDA income — the mismatch is automatic evidence of non-disclosure.

The Enforcement Machinery: How Non-Compliance Gets Detected

The theoretical penalties matter less than the practical probability of detection. That probability has increased sharply since 2022.

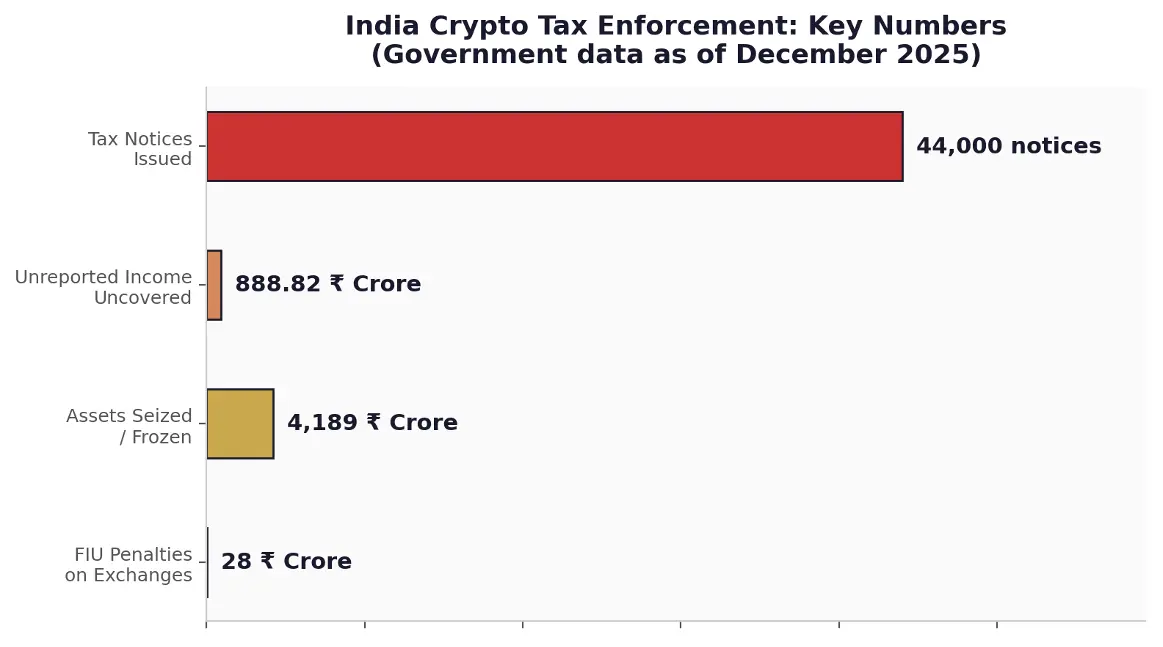

Figure 2: India crypto tax enforcement key numbers. Source: Government of India data, Parliament statement (December 2025).

The detection mechanisms are layered:

TDS trail under Section 194S. Every registered exchange deducts 1% TDS and reports it to the government via Form 26QE. The Income Tax Department uses Project Insight — its data analytics platform — to match these TDS filings against individual ITRs. If the TDS record shows a transaction but the ITR does not, the mismatch is flagged automatically.

FIU-IND reporting. All 49 FIU-registered crypto exchanges must file suspicious transaction reports (STRs) and cash transaction reports (CTRs) under the PMLA. From January 2026, crypto holdings fall within the definition of reportable financial assets under Rules 114F, 114G, and 114H — requiring institutions to share user data with tax authorities, similar to mutual funds and stocks.

Section 148A reassessment notices. In April 2026, the Income Tax Department began issuing Section 148A notices to crypto investors for transactions from FY 2021–22 onward. These notices can reopen assessments up to 3 years after the assessment year — or up to 10 years if escaped income exceeds ₹50 lakh. The Department’s risk engines can flag entire transaction volumes rather than actual profits, requiring the taxpayer to provide documentation proving the actual gain.

Total TDS collected rose from ₹157.9 crore in FY 2022–23 to ₹511.83 crore in FY 2024–25. At a 1% TDS rate, this implies total tracked crypto trading volume of approximately ₹51,180 crore in FY 2024–25. The government has a comprehensive view of who is trading — the question is whether those traders are reporting.

Budget 2026: New Reporting Penalties

The Union Budget 2026 introduced a new penalty framework under Section 446 of the Income Tax Act, 2025, targeting crypto reporting entities — exchanges and platforms registered under PMLA.

Obligation | Penalty | Who It Applies To |

Failure to furnish VDA transaction statement under Section 509(1) | ₹200 per day of default | Reporting entities (exchanges) |

Furnishing inaccurate information or failure to correct errors | ₹50,000 flat penalty (~$545) | Reporting entities (exchanges) |

These penalties apply to exchanges, not retail investors directly. But they tighten the reporting infrastructure further. As exchanges face penalties for inaccurate reporting, the data flowing to the Income Tax Department becomes more reliable — which in turn makes it harder for individual investors to avoid detection.

The 30% tax rate, 1% TDS, and loss set-off restrictions remain unchanged in Budget 2026. Despite industry requests for relief, the government has chosen enforcement over concession.

Exchange-Level Enforcement: FIU-IND Actions

The enforcement extends beyond individual taxpayers to the platforms themselves. FIU-IND imposed aggregate penalties of ₹28 crore on non-compliant VDA service providers during FY 2024–25.

Exchange | Action | Penalty / Outcome |

Binance | Operating without PMLA registration | ₹18.82 crore fine (June 2024); registered after payment |

Bybit | Operating without registration | ₹9.27 crore fine (January 2025); registered after payment |

KuCoin | Non-compliance | Registered in 2024 following penalty |

Coinbase | Compliance requirement | Completed FIU registration early 2025 |

25 offshore platforms | Blocking orders issued October 2025 | Apps and websites directed to shut down |

The FIU actions are relevant to individual investors because trading on unregistered exchanges does not reduce tax liability — it increases legal risk. Transactions on unregistered platforms still generate taxable income, but the lack of TDS deduction means the investor bears full responsibility for advance tax payments, and the absence of exchange-generated Form 26AS data makes compliance more difficult, not less.

Staying Compliant: A Practical Framework

Avoiding the penalty cascade requires four actions, none of which are complex.

Action | Detail | Deadline |

Report all VDA income in ITR | Use Schedule VDA in ITR-2 or ITR-3 | July 31 (or October 31 for audit cases) |

Pay advance tax | 15% by June 15, 45% by Sept 15, 75% by Dec 15, 100% by March 15 | Quarterly deadlines |

Verify TDS in Form 26AS / AIS | Match exchange TDS deductions with your records | Before filing ITR |

Maintain transaction records | Cost of acquisition, date, exchange, wallet address | Ongoing |

If you have unreported crypto income from prior years, the Income Tax Act allows updated returns under Section 139(8A) for up to 24 months from the end of the relevant assessment year. An additional tax of 25% (within 12 months) or 50% (within 24 months) of the aggregate tax and interest applies — but this is substantially less than the penalty and prosecution risk of being caught through a Section 148A notice.

Managed crypto investment platforms, like Grade Capital, that operate through registered, tax-compliant infrastructure handle TDS deduction, transaction record-keeping, and reporting automatically. This does not eliminate the investor’s responsibility to declare income and pay tax — but it eliminates the most common compliance failures: missing TDS, incomplete records, and untracked transactions.

This content is for informational and educational purposes only and does not constitute legal or tax advice. Consult a qualified tax professional for advice specific to your situation. Tax laws are subject to change.