Most chartered accountants treat all cryptocurrency under Section 115BBH — the flat 30% tax on Virtual Digital Assets. That is a costly simplification. Crypto derivatives, Bitcoin ETFs, staking rewards, and TDS refunds each follow entirely different tax provisions, and applying 115BBH uniformly can mean clients overpay by lakhs or, worse, face compliance action for misclassified income. Here are the seven CA crypto tax mistakes India's tax framework exposes most frequently — and the correct treatment backed by Income Tax Act provisions, CBDT circulars, and Ministry of Finance data from FY2024-25.

Mistake 1: Applying Section 115BBH to All Crypto Income

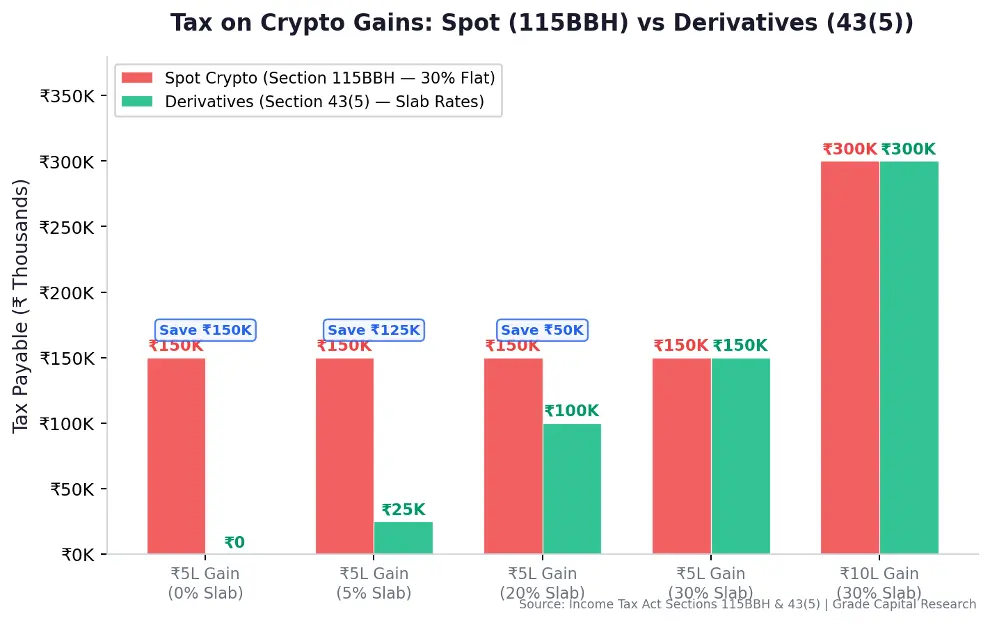

The most widespread error. Section 115BBH, introduced by the Finance Act 2022, imposes a flat 30% tax (plus cess) on income from the transfer of Virtual Digital Assets (VDAs). But VDA is a defined term — it covers spot crypto transactions. Crypto derivatives — futures and options contracts — do not involve the "transfer" of a VDA. They are settled in cash and classified as speculative business income under Section 43(5), read with Section 73 of the Income Tax Act.

The practical difference is enormous. Under 115BBH, a Rs 5 lakh gain attracts Rs 1,50,000 in tax regardless of your income level. Under Section 43(5), the same Rs 5 lakh gain could attract zero tax if your total income falls within the nil slab under the new regime (Section 115BAC), or just Rs 25,000 at the 5% slab.

Parameter | Spot Crypto (115BBH) | Derivatives (43(5)) |

Tax Rate | Flat 30% (+ 4% cess) | Slab rates (0% to 30%) |

Loss Set-off | Not allowed | Against speculative gains |

Loss Carry-forward | Not allowed | 4 years (speculative losses) |

Expense Deduction | Only cost of acquisition | All business expenses deductible |

ITR Form | ITR-2 (Capital Gains) | ITR-3 (Business Income) |

Surcharge | Applicable on gains | Applicable on total income |

TDS (Section 194S) | 1% on consideration | Not applicable |

Figure 1: Tax on crypto gains across income slabs — Spot (115BBH) vs Derivatives (43(5)). Source: Income Tax Act Sections 115BBH and 43(5)

Mistake 2: Assuming Crypto Losses Can Be Set Off Against Other Income

Some CAs still advise clients that crypto losses can offset equity or business income. Under Section 115BBH(2), losses from VDA transfers cannot be set off against any other income — not salary, not equity gains, not even gains from a different VDA. This is one of the strictest loss provisions in the entire Income Tax Act. A comparative analysis published in IJFMR (January 2026) noted that India's no-offset regime is significantly more restrictive than the US, UK, and Australia, all of which permit crypto losses to offset other capital gains.

Here is the critical nuance: this restriction applies only to spot VDA transactions under 115BBH. Derivative losses under Section 43(5) follow standard speculative business income rules — they can be set off against speculative gains and carried forward for 4 years. If your client trades both spot and derivatives, the classification determines whether a loss is dead weight or a usable deduction.

Mistake 3: Filing Bitcoin ETF Gains Under Section 115BBH

With BlackRock's iShares Bitcoin Trust (IBIT) and other US-listed spot Bitcoin ETFs now accessible to Indian investors through the Liberalised Remittance Scheme (LRS), a common mistake is treating ETF gains as VDA income under 115BBH. They are not.

A Bitcoin ETF is a regulated financial instrument traded on a recognised stock exchange (NYSE, NASDAQ). It is classified as a foreign asset for Indian tax purposes. As Treelife's analysis confirms, gains on Bitcoin ETFs attract 12.5% LTCG tax after a 24-month holding period — less than half of the 30% rate under 115BBH. Short-term gains (under 24 months) are taxed at slab rates, which can still be lower than 30% depending on the investor's total income. BusinessToday's Budget 2025 analysis confirmed that the government retained this treatment despite proposals to bring ETFs under the VDA framework.

LRS limits apply: $250,000 per financial year per individual, with 20% TCS above Rs 7 lakh (claimable as tax credit at filing).

Mistake 4: Missing the Double Taxation on Staking and Airdrops

Staking rewards and airdrops create a unique double taxation scenario that many CAs either ignore or mishandle. When you receive staking rewards, the fair market value at the time of receipt is taxable as income at your slab rate (since there is no cost of acquisition, the entire value is income). When you subsequently sell those tokens, the gain — measured from the FMV at receipt — is taxed again at 30% under Section 115BBH.

Example: You receive staking rewards worth Rs 50,000. You pay slab-rate tax on Rs 50,000 immediately. Six months later, the tokens appreciate to Rs 75,000 and you sell. The Rs 25,000 gain is taxed at 30% (Rs 7,500 + cess). Effective total tax on Rs 75,000 of economic gain: the slab-rate amount plus Rs 7,500 — potentially exceeding 40% combined. This is the only asset class in India where receipt and disposal are both independently taxed without any integration mechanism.

CAs should document the FMV at receipt meticulously — this becomes the cost basis for the subsequent 115BBH computation, and missing it can lead to the entire sale value being treated as gain.

Mistake 5: Ignoring the TDS Refund Opportunity Under Section 194S

Section 194S mandates a 1% TDS on the transfer consideration (not profit) for VDA transactions exceeding Rs 10,000 per year (Rs 50,000 for specified persons). The Ministry of Finance disclosed that Rs 511.83 crore in TDS was collected under Section 194S in FY2024-25.

What most CAs miss: 1% TDS on consideration is almost always more than the actual tax liability as a proportion of each trade. If a trader buys crypto at Rs 1,00,000 and sells at Rs 1,05,000, TDS deducted is Rs 1,050 (1% of sale). Actual tax on the Rs 5,000 gain is Rs 1,500 (30%). But the TDS was on the full consideration, not the gain. For high-frequency traders with thin margins, TDS deducted can significantly exceed actual tax liability — creating a refund opportunity at ITR filing. CAs who simply ignore TDS certificates or fail to claim credit leave money on the table.

Mistake 6: Ignoring Offshore Exchange Compliance Risk

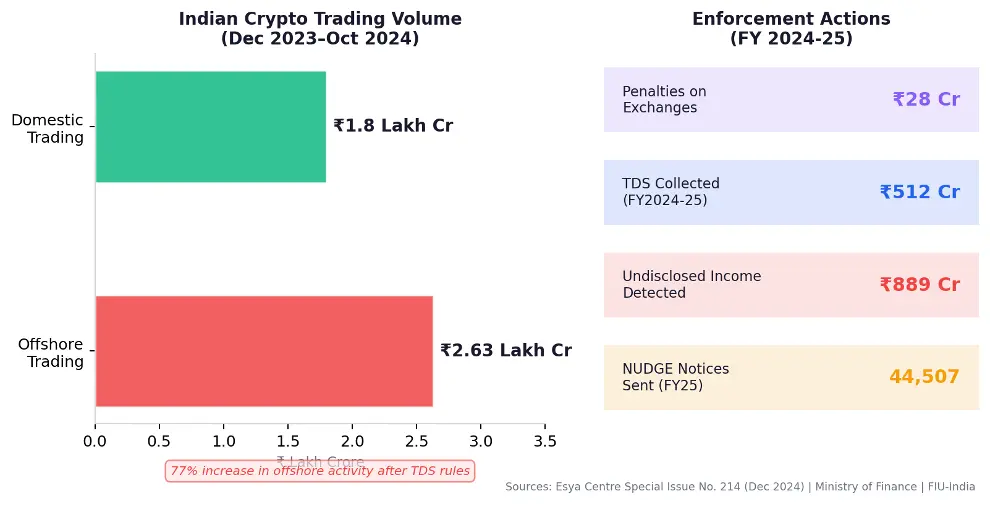

This is where the stakes are highest. According to the Esya Centre's Special Issue No. 214 (December 2024), Indians traded Rs 2.63 lakh crore on offshore platforms between December 2023 and October 2024 — exceeding domestic trading volume. Offshore activity increased 77% from January to October 2024, driven partly by traders migrating to avoid the 1% TDS.

Figure 2: Indian crypto trading volumes — offshore vs domestic (Dec 2023–Oct 2024). Sources: Esya Centre Special Issue No. 214, Ministry of Finance, FIU-India

The enforcement response has been substantial. According to Ministry of Finance parliamentary disclosures compiled by KoinX: the Income Tax Department sent 44,507 NUDGE notices to crypto holders in FY2024-25, detected Rs 888.82 crore in undisclosed crypto income, and FIU-India imposed Rs 28 crore in penalties on non-compliant exchanges including an Rs 18.82 crore fine on Binance.

What CAs need to know now: CBDT's March 2026 amendment to Rules 114F, 114G, and 114H brings crypto under FATCA/CRS reporting. This means exchanges will share data with Indian tax authorities automatically. The OECD's Crypto-Asset Reporting Framework (CARF) takes this further — 67 jurisdictions have committed to automatic exchange of crypto transaction data, with India committed to first exchanges by 2027. Additionally, Budget 2025 introduced Section 158B block assessment provisions allowing 60% tax plus 50% penalty on unreported crypto income discovered during search and seizure operations. The Esya Centre estimates that cumulative uncollected TDS from offshore platforms exceeds Rs 6,000 crore, with a projected Rs 17.7 lakh crore in offshore trading over the next five years — translating to Rs 17,700 crore in uncollected TDS.

CAs advising clients who have traded on offshore exchanges should proactively review disclosures before the CARF data-sharing pipeline goes live in 2027. CBDT Circular No. 13/2022 clarifies that individual users are responsible for TDS compliance on offshore platforms — the exchange's non-compliance does not absolve the taxpayer. As of 2026, only 49 VASPs are registered with FIU-India, and KuCoin remains the only FIU-registered offshore platform deducting TDS, accounting for less than 5% of offshore volume.

Enforcement Metric | FY 2024-25 Data | Source |

TDS Collected (Section 194S) | Rs 511.83 crore | Ministry of Finance |

NUDGE Notices Sent | 44,507 | Income Tax Department |

Undisclosed Income Detected | Rs 888.82 crore | Ministry of Finance |

Penalties on Exchanges | Rs 28 crore | FIU-India |

Binance Fine | Rs 18.82 crore | FIU-India |

Registered VASPs | 49 | FIU-India |

Offshore Trading Volume | Rs 2.63 lakh crore | Esya Centre |

Projected 5-Year Offshore Volume | Rs 17.7 lakh crore | Esya Centre |

Mistake 7: Not Advising Clients on the Derivatives Tax Advantage

This is perhaps the most consequential gap in CA advice today. The tax difference between spot and derivatives is not a loophole — it is the intended legislative design. Section 115BBH was specifically drafted for VDA transfers. Derivatives settled in cash are speculative business income. The classification is clear in the statute.

For a salaried professional earning Rs 10 lakh per annum, a Rs 5 lakh gain from spot crypto attracts Rs 1,50,000 in tax. The same gain from managed crypto derivatives at the 15% slab bracket would attract Rs 75,000 — a 50% reduction in tax outgo. At lower slabs, the difference is even more dramatic. Under the new tax regime (Section 115BAC), income up to Rs 12 lakh is effectively tax-free thanks to the Rs 75,000 standard deduction and rebate under Section 87A — meaning derivative income within this threshold could attract zero tax compared to the flat 30% on spot.

Beyond the rate difference, derivatives offer three structural advantages that spot crypto simply cannot match: deduction of business expenses (trading fees, software, internet), set-off of losses against other speculative gains, and carry-forward of unused losses for 4 years under Section 73.

A Structural Alternative Worth Considering

The derivatives tax advantage is not theoretical — managed crypto derivatives platforms like Grade Capital are structured specifically around Section 43(5). Instead of buying and selling spot crypto (triggering 115BBH), these platforms deploy professionally managed derivatives strategies — futures and options on BTC and ETH — where gains are classified as speculative business income at slab rates. The strategy includes hedged positions that can deliver returns even in falling markets.

Figure 4: Grade Capital's managed crypto baskets — Gold and Blue Chip (100% profit, XIRR +75%), goal-based planning for retirement, starting at Rs 12,000. Source: Grade Capital app

For CAs advising clients who are already in crypto or considering allocation, the question is not whether crypto income is taxable — it is. The question is which classification yields the most tax-efficient outcome for the client. Section 43(5) derivatives and LRS-route Bitcoin ETFs are both legitimate, lower-tax alternatives to spot trading under 115BBH.

The Bottom Line

India's crypto tax framework is more nuanced than a single section. CAs who stop at 115BBH risk overstating their clients' tax liability, missing legitimate deductions, and leaving TDS refunds unclaimed. With CARF data-sharing approaching in 2027, 44,507 NUDGE notices already sent, and Section 158B's 60% penalty for undisclosed income, the cost of getting crypto tax wrong — in either direction — has never been higher.

The seven mistakes outlined here are not edge cases. They cover the most common scenarios CAs encounter: spot vs derivatives, ETFs, staking, TDS credits, and offshore compliance. Addressing them requires no special expertise — just a careful reading of the existing statute.

Want to understand how managed crypto derivatives can fit into your clients' portfolios? Explore the Grade Capital Knowledge Hub for detailed guides on tax-efficient crypto investing.

Disclaimers

This article is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Readers should consult qualified professionals before making investment or tax-filing decisions.

Past performance is not indicative of future results. Cryptocurrency markets are volatile and subject to regulatory changes. All performance data cited in this article refers to historical observations and should not be construed as projections or forecasts.

Tax treatment depends on individual circumstances and the prevailing interpretation of tax laws. The classification of crypto derivatives as speculative business income under Section 43(5) is based on current statutory reading and may be subject to future CBDT clarifications or amendments.

All data, statistics, and enforcement figures are sourced from publicly available government disclosures, research publications, and tax guides as cited. While every effort has been made to ensure accuracy, readers should verify current provisions independently. Projections cited from the Esya Centre and other sources are estimates and not forecasts.

Grade Capital is a managed crypto derivatives platform. Mention of Grade Capital in this article is for illustrative purposes. Investment decisions should be based on individual due diligence.